If the price of tents should increase then it would cause the demand for sleeping bags to reduce.

<h3>What is a complementary good?</h3>

This is the term that is used to refer to the goods that are bought and used alongside another good. What this means is that both goods are used together.

Hence when the price of one complement good rises, it would cause the demand of that good to reduce and also reduce the market for that good.

Read more on complement goods here: brainly.com/question/1338465

#SPJ1

Answer:

Greg eats pizza every day of the week. The marginal utility of pizza will most likely <u>decrease </u> by the end of the week, and all else being equal, this demonstrates the law of <u> diminishing marginal </u><u>utility</u><u> </u><u>.</u>

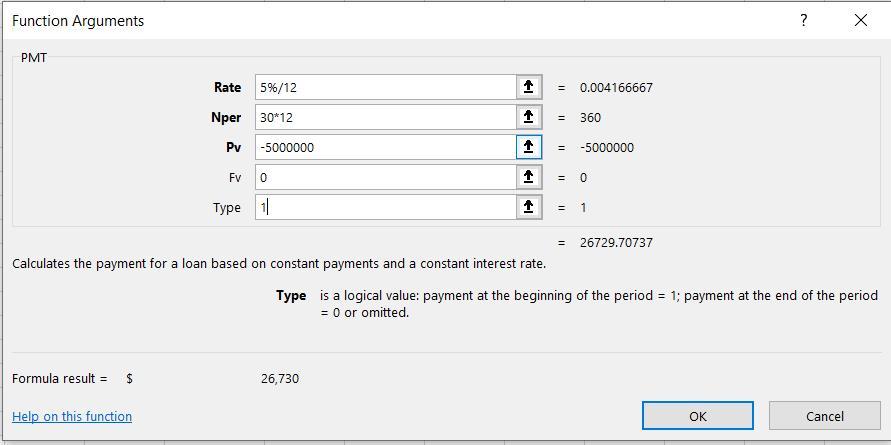

Answer:

$26,730

Explanation:

The explanation for this question is given in the attachment below.