Answer: c. Is equal to the market value of the land

Explanation:

When deciding the cost of using an asset such as land for something, the best cost to use is the opportunity cost of the land. What would the US Government be doing with the land if they were not turning it for use for the black-tailed prairie doga.

As there are no other alternatives, this cost will therefore be the market value of the land because this is the amount that the Government could get for the land if they sold it instead of using it for the black-tailed prairie doga.

Answer:

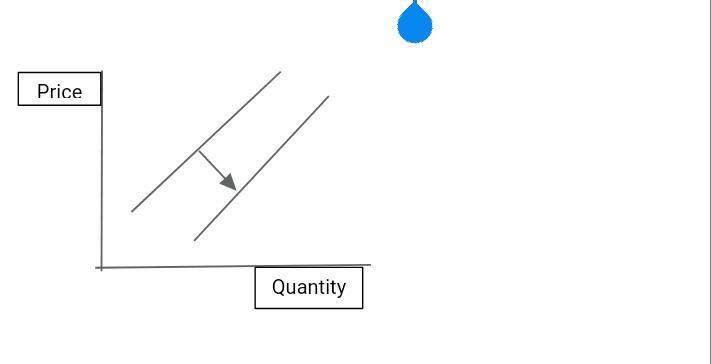

A. shifted to the left

Explanation:

When refineries shut down,the supply of oil would reduce. This would lead to a shift of the supply curve to the left.

I hope my answer helps you

Answer:

Entrepreneurship is important, as it has the ability to improve standards of living and create wealth, not only for the entrepreneurs but also for related businesses. Entrepreneurs also help drive change with innovation, where new and improved products enable new markets to be developed.

Answer:

$69,000 per year

Explanation:

the total economic cost of going to college = college expenses + implicit costs

- college expenses = $30,000

- implicit costs (opportunity costs) = $45,000 x 2 = $90,000

total economic cots = $30,000 + $90,000 = $120,000 / 5 years

if you want to recover your college costs in 5 years, you will need to recover $120,000 / 5 = $24,000 per year

so you would need to earn = $45,000 (old salary) + $24,000 = $69,000 per year

*opportunity costs are the additional costs or benefits lost from choosing one activity or investment over another alternative.

Explanation:

The journal entry to record the re-issuance of the stock is shown below:

Cash A/c Dr $240,000 (20,000 shares × $12)

Retained earnings A/c Dr $80,000

To Treasury stock $320,000

(Being the re-issuance of the stock is recorded)

The computation is shown below:

For treasury stock

= 20,000 shares × ($16 per share - $12 per share)

= $80,000

So as we can see the retained earnings is decreased by $80,000