Answer:

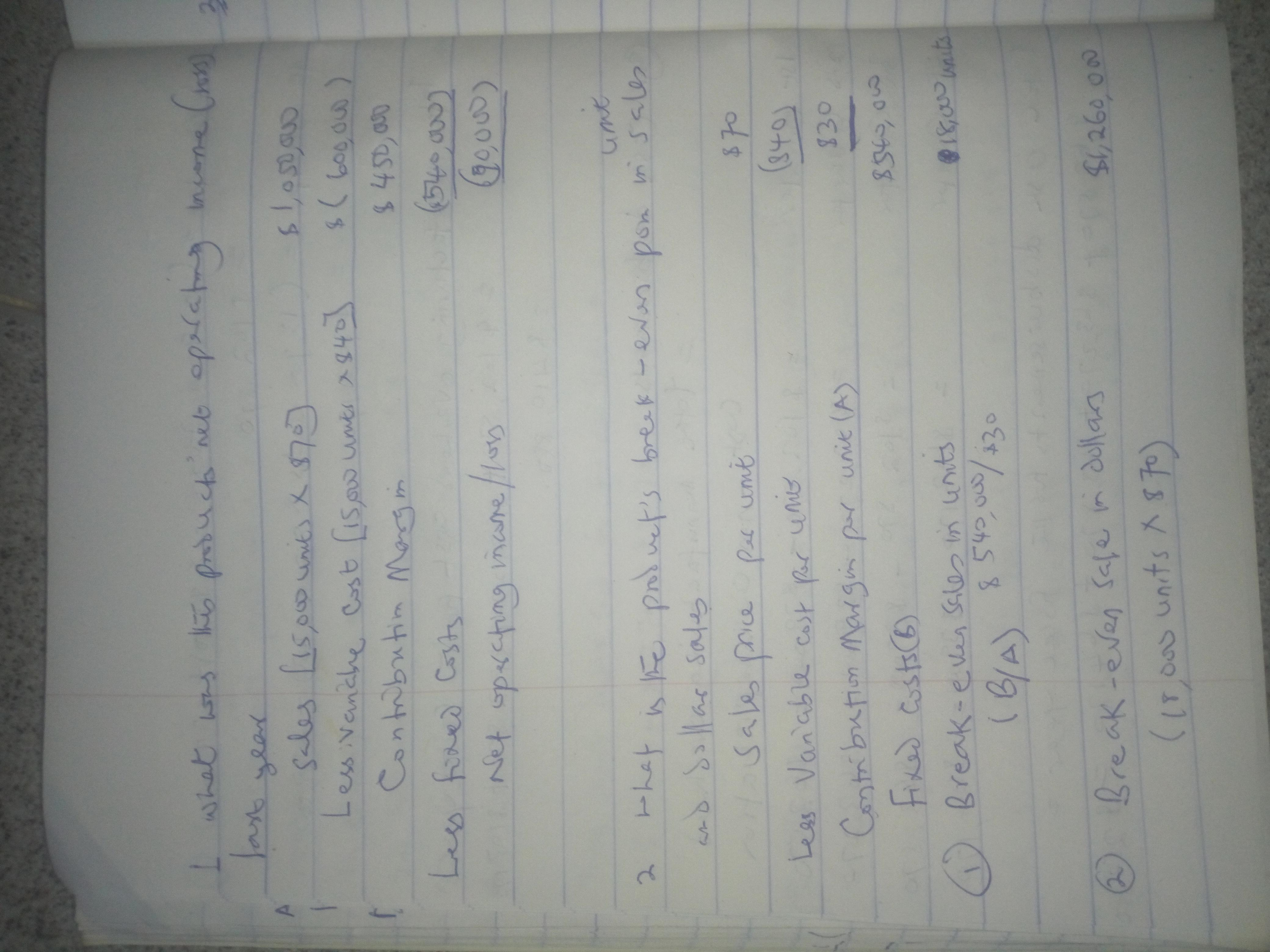

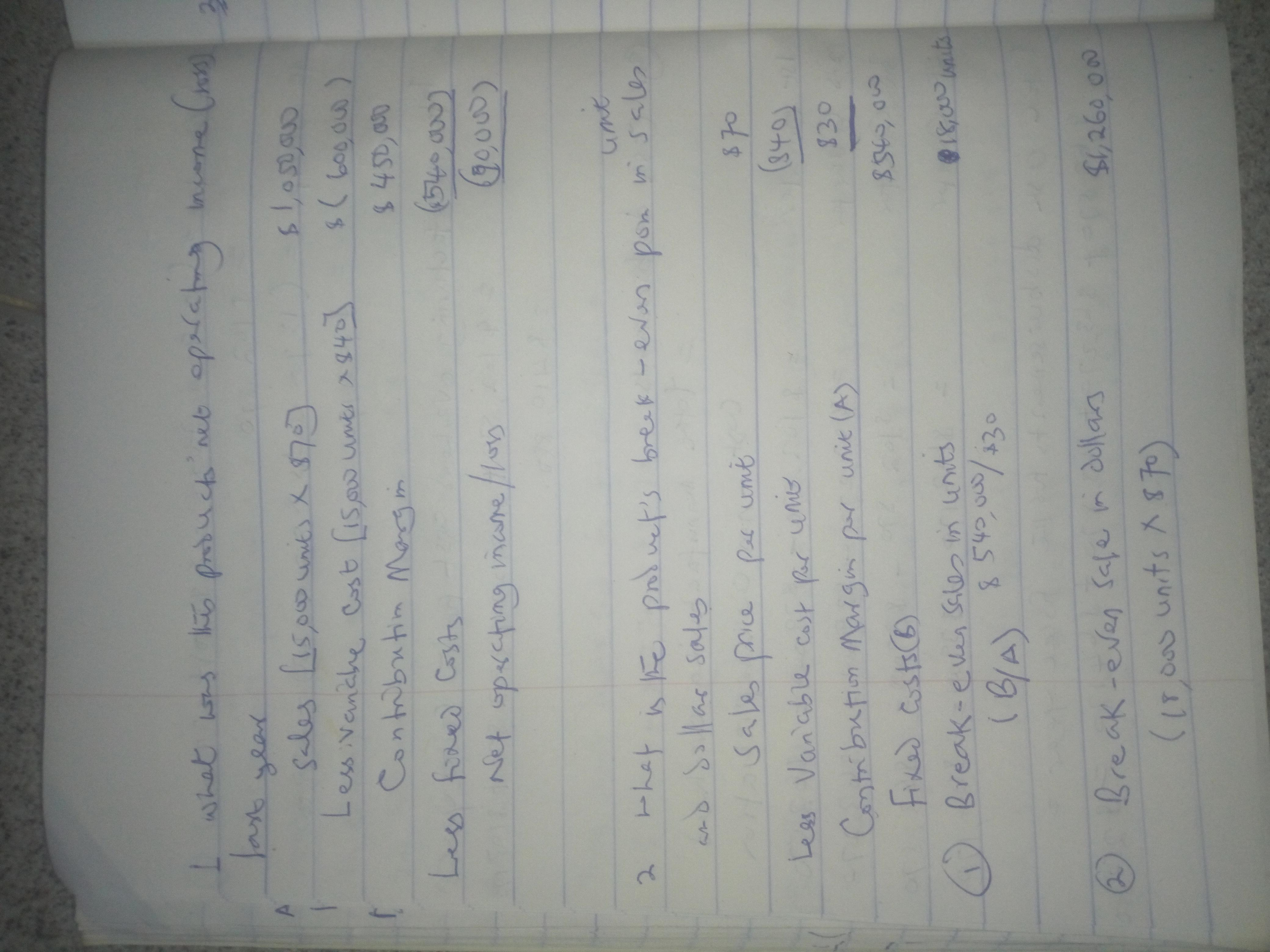

1. What was the product's operating income(loss) last year = $90,000 loss

2. What is the product's Break even point in unit sales and dollars

• Break even sales in units 18,000

• Break even i n sale dollars $1,260,000

3. Maximum annual profit given an increment of 5,000 units and reduction of sales price per unit by $2.

• Net profit of $20,000

4. What would be the break even point in unit sales and dollars using the selling price that you determined in requirement 3.

• Break even sales units 19,285.7

• Break even in sales dollars $1,311,427.6

Explanation:

Please see attached detailed solution to the above questions and answers.