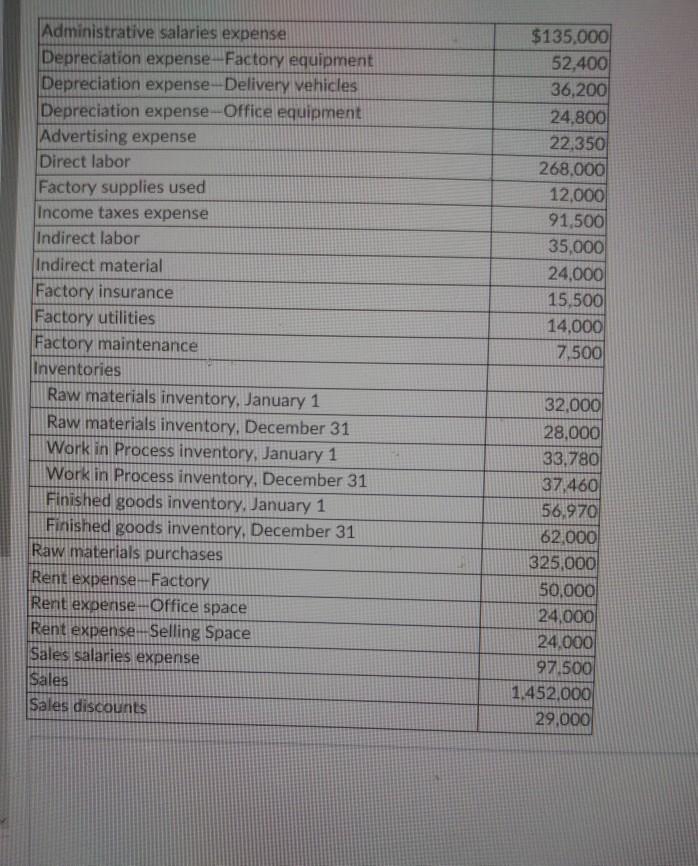

Answer: hello your question is incomplete attached below is the missing data. ( first image )

answer:

Attached below

Explanation:

A) company's schedule of cost of goods manufactured for year ended

attached below is the required schedule ( second Image )

B) Company's income statement

attached below is the company's income statement ( Image 3 and 4 )

Explanation:

Beginner, Apprentice, Rising Star, Helping Hand, Ambitious, Virtuoso, Expert, Ace, Genius,etc

Answer:

Option B

Explanation:

Fixing the wage rate above the market equilibrium rate will disturb the demand and supply equilibrium of labor resource.

Wage rate above market will make labor as a resource costly for business and hence, there is possibility that the demand for labor will lower down. Thus, the supply of labor will get low.

Hence, option B is correct

Answer:

Cost of goods manufactured

Explanation:

Cost of goods manufactured are reported on the face of income statement because it's a critical factor in arriving at the profit or loss position at the end of a period. Cost of goods manufactured takes cognizance of the material costs, labour and overhead costs involved in production. This determines the overall financial status of a company, and allow a decision maker to know if the business is doing good or not.

Answer:

The correct answer is Information search

Explanation:

Before deciding on the first offer, it is necessary to review or look for other options in order to have a better view of the options and be able to decide on one that offers the best utilities for what is needed. In this case Tom carries out a search process in order to know the options offered in the market and to be able to have an accurate decision according to his needs.