Answer:

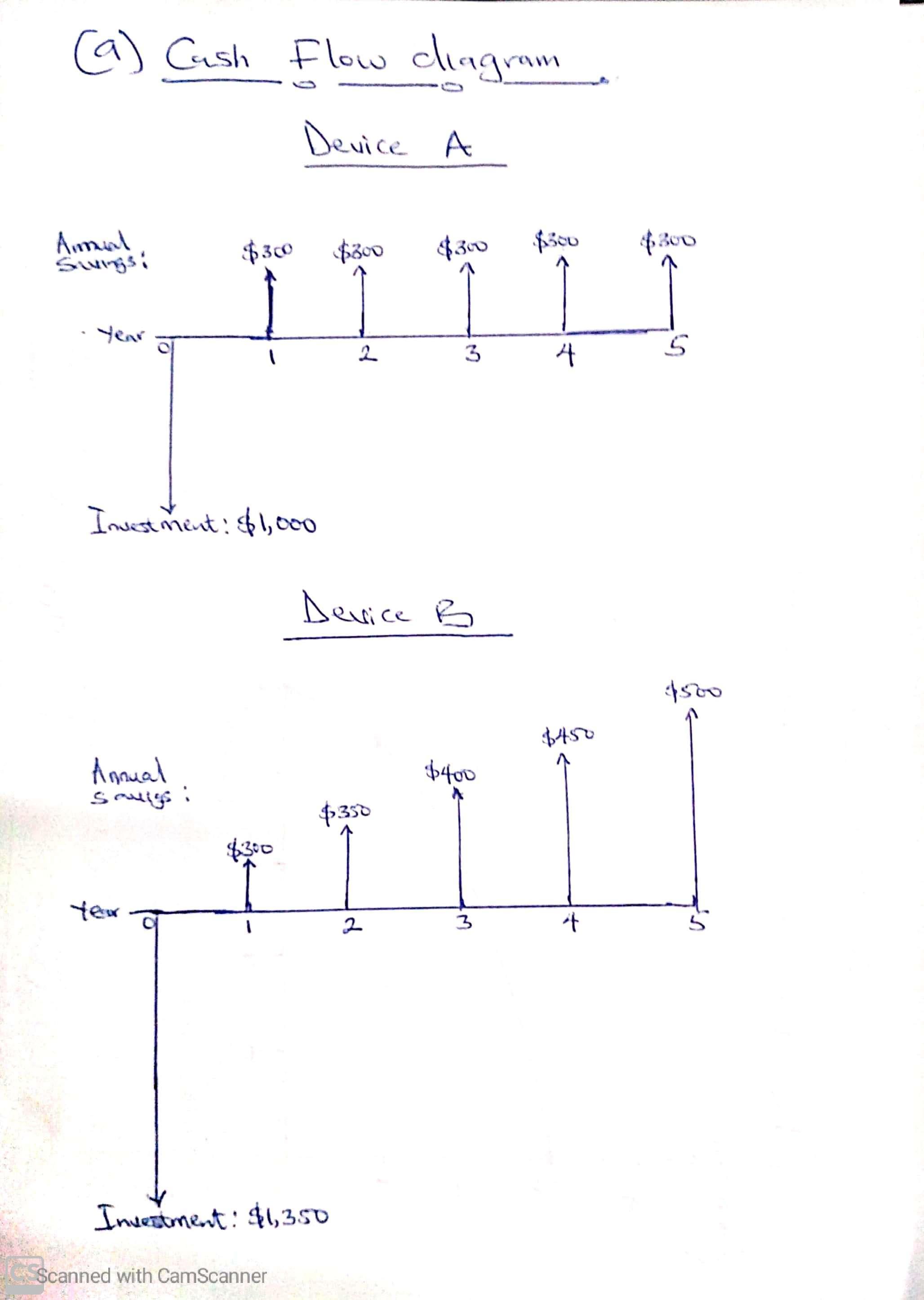

a) Find the attached jpeg file for the cash flow diagram

b) The company should purchase Device B.

Explanation:

a) Draw cash flow diagram for each option

A project cash flow diagram is a tool that is used to present a visual representation of the cost of a project and cash it is expected to generate over a specified period of time. On the diagram, x-axis represents the year, and y-axis represents cash out flows and/or inflows.

Note: See the attached jpeg for the cash flow diagram.

b) If interest rate is 7%, which device should your company purchase?

To determine this, we compare the Net Present Value (NPV) of the 2 devices.

Note: See the attached excel file for the calculation of the NPVs of the two devices.

From the attached excel file, we have:

NPV of Device A = $230

NPV of Device B = $262

Decision: Since $262 NPV of Device B is greater than the $230 NPV of Device A, <u>the company should purchase Device B.</u>

Answer:

$10,000.

The investment is written down to fair value, and the impairment loss is recognized in net income.

Explanation:

Given that

Purchase value of the bond = $100,000

Decline value = $70,000

Decrease in fair value = $30,000

Credit losses = $10,000

Non credit losses = $20,000

Based on the above information, the before tax net income for year 2016 is reduced by $10,000 as Nicholds wants to hold the bond till maturity date. So the non credit part of decrease in fair value would not be adjusted

Therefore only credit losses should be relevant

As it is mentioned in the question that the debt investment fair value is to be considered as an available-for-sale investment and viewed as an other than temporary therefore the written down of investment to fair value and the loss of impairment should be recorded in the net income

Answer:The answer is a

Explanation:

A contract is an agreement between two or more parties which contains the terms and conditions of the contract and which also serve as an evidence that the two parties in the contract has a duty to perform to each other. The terms and conditions of the contract can be enforced in the court of law in case of a breach of contract which may come from either parties in the contract agreement. While, a contract interference is a kind of breach of contract in which one vendor put a pressure on the organization in which they offer service to withdraw from the contract the organization earlier had with one of their competitors in the market. This contract interference can occur when a vendor either force or put a financial inducement on the organization with a view to make them consider their proposal to the organization to eventually agree to abandon the contract they had with their competitors in favour of getting the contract instead of their competitors who should get the contract.

Therefore, from what we can deduce from the question under review, it is clear that A plus linen has engage in contract interference by offering John C Lincoin hospital $5 for every 100 pound of linen they send to them by dropping their current linen service.

The answer to this question is diffusion. Diffusion is an act of spreading information or message from one person to another. Diffusion is also called dispersal. Diffusion in business is a term which means spreading of new business ideas such as new products that is acceptable in the market or to consumers.

Answer:

a) Competitive price

Explanation:

a) Competitive price

Competitive price strategy is taken into consideration for setting prices for a product keeping in mind the competitors price for the similar products.

Competitive price have better sales and compete better with other similar products in the market. It gains a competitive edge in the market. It gains maximum customer recognized values.