The ethics trap that is faced here would be contemplating to accept the reallocation because rejecting it may mean trouble and even lead to a lose of our jobs.

<h3>What is meant by ethical trap?</h3>

This is the term that has to do with the circumstances that may lead an individual to do away with the core values and the principles that they have. The trap here is that I may lose my job or may not have any bonus but accepting is going against the ethics and the values that I may hold special.

What should have been in this situation would have been to come clean in the first place so as to avoid going against ethics and the principles of the profession. The best way to do this would be to go to the head of division and explain the situation at hand to him.

Hence we can say that The ethics trap that is faced here would be contemplating to accept the reallocation because rejecting it may mean trouble and even lead to a lose of our jobs.

Read more on ethics here:

brainly.com/question/13969108

#SPJ1

<span>Oriental trading company will be more effective if it has a mechanistic structure.

According to Burns and Stalker who came up with this term, mechanistic structure involves </span><span>organizational complexity, formalization, and centralization. It is the type of structure which best fits the description given above.</span><span>

</span>

Answer:

A - shifting the aggregate demand curve to the left, reducing real GDP and lowering the price level

D - consumption, investment, and net exports decrease; aggregate demand decreases.

Explanation:

If interest rates increase, it becomes more expensive to borrow money (since there is a larger amount to be paid back on top of the value of the loan) and more beneficial to save money (since banks will pay more for saving). This means that consumers are less likely to take out loans and more likely to store their money in the bank, leading to a reduction in consumption—less consumer spending, more saving. Likewise with firms, which will be less likely to invest in new capital (because borrowing funds to buy it costs more) and more likely to save profits. This reduction in consumption and investment means that aggregate demand falls, represented in a diagram by a shift to the left.

Thanks

Answer:

The correct option is D

There is increase in ROE by 2.86%

d. 2.86%

EXPLANATION:

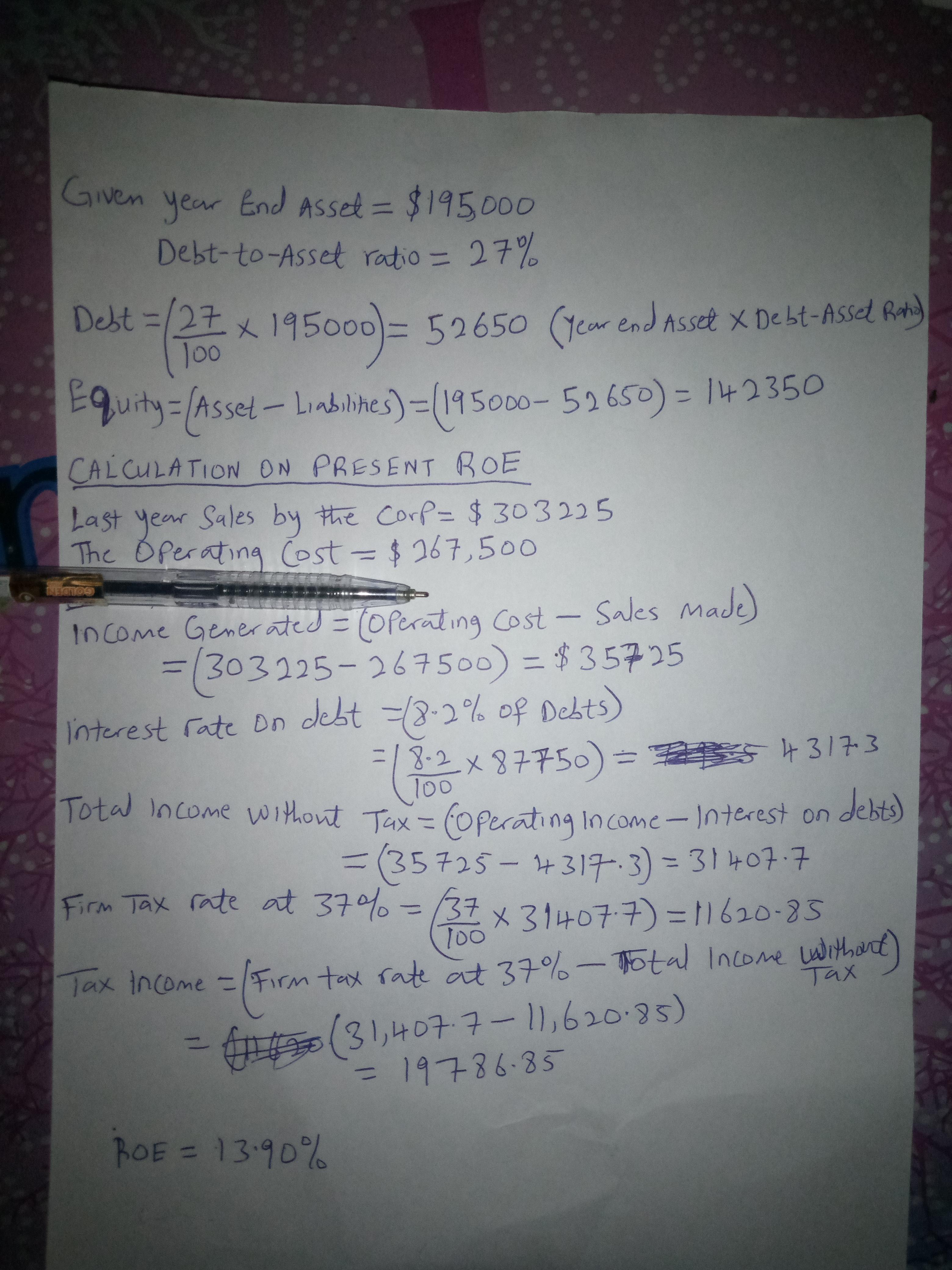

THIS IS THE COMPLETE QUESTION BELOW;

Last year Swensen Corp. had sales of $303,225, operating costs of $267,500, and year-end assets of $195,000. The debt-to-total-assets ratio was 27%, the interest rate on the debt was 8.2%, and the firm's tax rate was 37%. The new CFO wants to see how the ROE would have been affected if the firm had used a 45% debt ratio. Assume that sales and total assets would not be affected, and that the interest rate and tax rate would both remain constant. By how much would the ROE change in response to the change in the capital structure?

a. 2.08%

b. 2.32%

c. 2.57%

d. 2.86%

e. 3.14%

CHECK THE ATTACHMENT BELOW FOR DETAILED EXPLANATION

Answer:

See below

Explanation:

The amount of direct labor cost incurred is computed as;

= $30,000/$70,000 × $2,000

= $857

Overhead applied in ending working in the ending inventory of work in process on July 31

= $15,000/$70,000 × $2,000

= $429