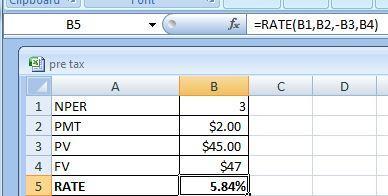

Answer:

5.84%

Explanation:

We use the RATE function that is shown in the excel. Kindly find the attachment below:

The NPER shows the time period.

Given that,

Present value = $45

Future value or Face value = $47

PMT = $2

NPER = 3

The formula is shown below:

= Rate(NPER,PMT,-PV,FV,type)

So, the annual compound rate of return is 5.84%

Answer:

The correct answer is c. the exhaustion doctrine.

Explanation:

"Exhaustion" refers to one of the limitations of intellectual property rights. Once a product protected by an intellectual property right has been marketed by your SME or by others with your consent, your SME is no longer entitled to exercise the intellectual property rights of the commercial exploitation of this given product, since it They have "sold out." Sometimes this limitation is also called the "first sale doctrine", since commercial exploitation rights on a given product end with the first sale of the product. Unless the legislation specifically provides otherwise, your SME may not control or oppose subsequent acts of resale, rental, loan or other forms of commercial use by third parties. There is a fairly broad consensus that this applies at least within the framework of the national market.

Answer:

62,400 units

Explanation:

The computation of the equivalent units for conversion cost is shown below:

= Started and completed units × completion percentage + closing inventory units × completion percentage

where,

Started and completed units is

= 65,000 units - 6,500 units

= 58,500 units

So the equivalent units is

= 58,500 units × 100 + 6,500 units × 60%

= 58,500 units + 3,900 units

= 62,400 units

The 3/5 finished means 60% is finished

Answer:

The correct option is <u>b. irrelevant cost</u>.

Explanation:

An irrelevant cost can be described as an expense that will not be affected by the decisions of thee management. Therefore, irrelevant costs are those that will not change if you choose one option over another in the future.

Therefore, the $4,000 of annual operating costs that are common to both the old and the new machine are an example of irrelevant cost. This is because the 4,000 of annual operating costs will not be affected or will still be incurred whether Jarett Motors managment decide to keep its existing car washing machine or purchase a new one.

Therefore, the correct option is <u>b. irrelevant cost</u>.

Answer: Things to consider when creating a budget.

Explanation: Trust me bro