Answer:

Explanation:

Answer:

On Dec 31, 2012 Lee's liability would be $9,500 (principal amount) and $38 (accrued interest)

Explanation:

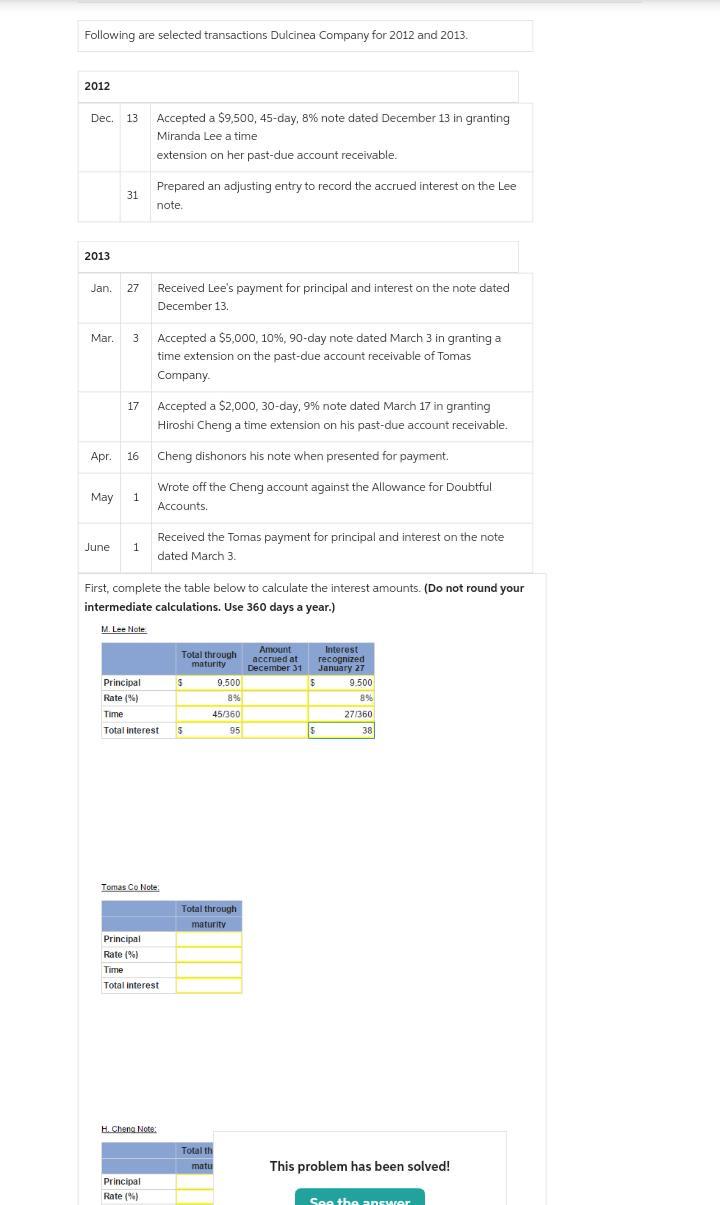

Lees notes:

Dec. 13 Accepted a $9,500, 45-day, 8% note dated December 13 in granting Miranda Lee a time extension on her past-due account receivable.

First interest due = $9,500 x 8% x 45/360 = $95

On the 31st 18 days would have accrued of the 45days = 18/45 x $95 = $38

On Dec 31, 2012 Lee's liability would be $9,500 (principal amount) and $38 (accrued interest)

Debit Miranda Lee with $9,538

Credit interest on Receivables $38

Credit Account receivables account with $9,500

When the full interest became due we will pass an additional entry:

Dr. Lee with $58

Cr. Interest on receivables with $58

(Being the balance interest on receivables due )

On Jan 27 when Lee paid her interest and principal amount, we will:

Debit Account receivables with $9,500

Debit interest on receivables Account with $95

Credit Tomas account with $9,595

( being liquidation of Lee's indebtedness)

Tomas notes:

Mar 3, Accepted a $5,000, 10%, 90-day note dated March 3 in granting a time extension on the past-due account receivable of Tomas Company.

Let's recognize the full interest due first:

$5,000 x 10% x 90/360 = $125

At this time we will:

Debit Tomas with $5,125

Credit interest on receivables with $125

Credit Account Receivables account with $5,000

On June 1 when Tomas paid his interest and principal amount, we will:

Debit Accounts receivable with $5,000

Debit interest on receivables with $125

Credit Tomas account with $5,125

( being liquidation of Tomas indebtedness)

Hiroshi Cheng notes:

Accepted a $2,000, 30-day, 9% note dated March 17 in granting Hiroshi Cheng a time extension on his past-due account receivable.

Interest = $2,000 x 9% x 30/360 = $15

The entries recognizing this liability will be to :

Debit Cheng Account with $2,015

Credit interest on receivables with $15

Credit Accounts receivable with $2,000

(Being receivables payable balance and interest on balance owed by Cheng)

However Cheng failed in paying up. It was decided to write off the debt.

The entries would be:

Dr. Accounts receivables $2,000

Dr. Interest on Accounts receivables with $15

Cr. Cheng's Account with $2,015

(Being debt owed by Cheng written off)