Answer:

the amount of the impairment loss is $50,000

Explanation:

The computation of the amount of the impairment loss is shown below:

Impairment loss = Purchase price of trade marks - Estimated fair value

= $70,000 - $20,000

= $50,000

Hence, the amount of the impairment loss is $50,000

The same should be considered and relevant

The annual percentage yield on Monty's default or penalty rate equals to 42.58%.

<h3>What is the meaning of APY?</h3>

APY is an acronym for Annual percentage yield.

The percentage yield referred to the real rate of return that is earned on an investment after taking into account the effect of compounding interest.

Given that the Visa card has an original default or penalty rate of 36%, the annual percentage yield on Monty's default or penalty rate equals to 42.58%.

Read more about annual percentage yield

<em>brainly.com/question/13012002</em>

#SPJ1

Answer:

The first part of the question was missing, so I looked for it:

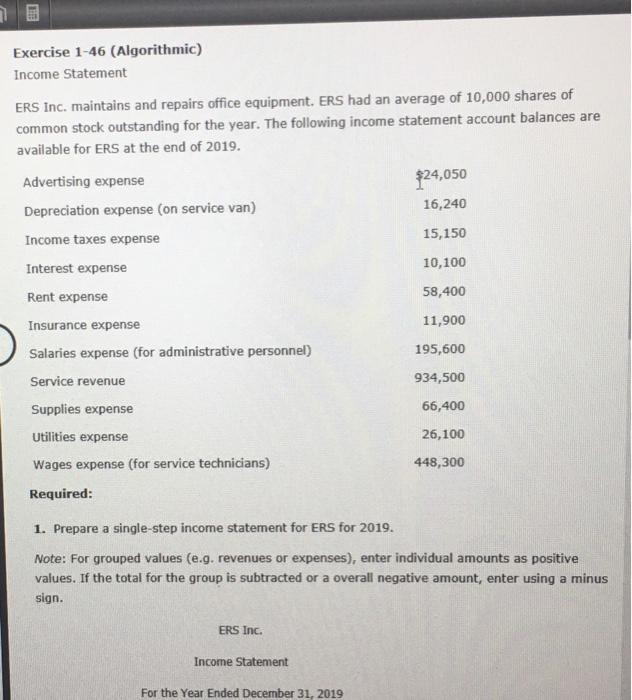

total revenue = $934,500

net income = $62,260

net profit margin = (net income / total revenue) x 100 = ($62,260 / $934,500) x 100 = 6.662%

if revenue increases by $100,000, then net income should increase by:

$100,000 x 6.662% = $6,662

Answer:

The transistor was invented on June 30th 1948 by Bell telephone laboratories

Answer:

Rate of return = 6.64%

Explanation:

Annual coupon rate = 7.5% = 0.075

Face value = 1,000

Coupon payment = 1,000*0.075 = 75

YTM = 8%

Years = 20

Price of the bond = PV(8%, 20, 75, 7.5%)

Price of the bond = $950.91

Rate of return = Selling price + Coupon payment received - Purchase price / Purchase price

Rate of return = $939.05 + $75 - $950.91 / $950.91

Rate of return = $63.14 / $950.91

Rate of return = 0.0663996

Rate of return = 6.64%