Answer:

The correct answer is (C) straight variable cost assumptions.

Explanation:

If the total cost increases with small increases in activity, it may be referred to as a step-variable cost.

Answer:

285,000 units

Explanation:

The computation of the cash break-even point of sales units is shown below:

Cash break-even point = (Fixed cost - depreciation) ÷ (contribution margin per unit)

where,

Fixed cost = $7,600,000

Depreciation = $7,600,000 × 0.25% = $1,900,000

And, the contribution margin per unit is $20

So, the cash break-even point of sales units is

= ($7,600,000 - $1,900,000) ÷ ($20)

= 285,000 units

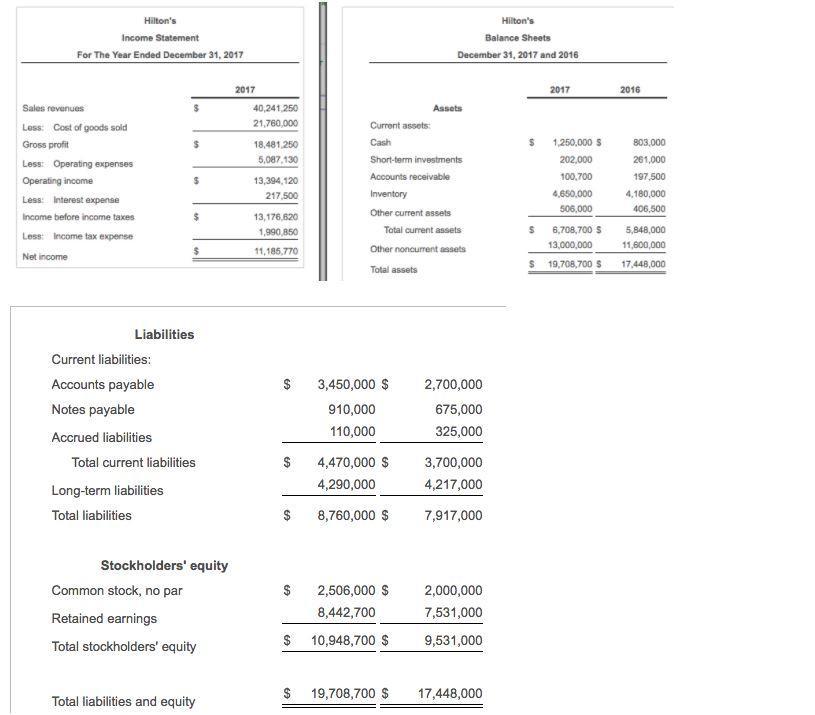

Answer:

a. 2017 ⇒ 1.50

2016 ⇒1.58

b. Deteriorate

Explanation:

a. Current ratio 2017

= Current Assets / Current liabilities

= 6,708,700 / 4,470,000

= 1.50

Current ratio 2016

= 5,848,000 / 3,700,000

= 1.58

b. The current ratio went from 1.58 in 2016 to 1.50 in 2017 which would mean that it deteriorated.

Answer:

a) 46.7, 80 b) 20, 60 c) yes

Explanation:

a) % utilization= utilization/design capacity × 100

= 7/15 × 100

= 46.7%

% efficiency= efficiency/design capacity × 100

= 12/15 × 100

=80%

b) Utilization= 2/10 × 100 = 20%

Efficiency= 6/10 × 100= 60%

c) A system with higher efficiency ratios will always have higher utilization as these systems will have lesses number of failures

Answer:

$850

Explanation:

Data provided in the question:

Initial investment = $15,000

Expected annual net cash flows over four years, R = $5,000

Return on the investment = 10% = 0.10

Present value of an annuity factor for 10% and 4 periods, PVAF = 3.1699

The present value of $1 factor for 10% and 4 periods = 0.6830

Now,

Net present value = [ R × PVAF ] - Initial investment

= [ $5,000 × 3.1699 ] - $ 15,000

= $15,849.50 - $ 15000

= $849.50 ≈ $850