Answer:

A. Measures the ending inventory at the actual prices of the specific units sold during the period

Explanation:

The Specific identification inventory costing method is a strategy of getting the actual ending inventory cost. To get this cost requires the deliberate manual calculation of each of the remaining commodities brought on certain dates, at year-end inventory. The number gotten is then multiplied by their actual cost of purchase date. The result is then taken as the ending inventory cost.

Consequently, the purpose is to allocates the specific cost of each inventory item to cost of goods sold.

Hence, in this case, the correct answer is option A. Measures the ending inventory at the actual prices of the specific units sold during the period.

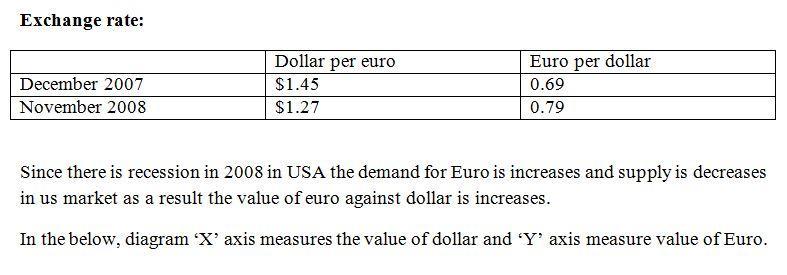

Answer

The answer and procedures of the exercise are attached in the following archives.

Step-by-step explanation:

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

Answer:

Statement 1: Explicit cost

Statement 2: Implicit cost

Statement 3: Implicit cost

Statement 4: Explicit cost

Accounting profit = Sales revenue - Explicit cost

= 722,000 - (422,000 + 268,000)

= $32,000

Economic profit = Sales revenue - (Explicit cost + Implicit cost)

= 722,000 - (422,000 + 268,000 + 2,000 + 21,000)

= $9,000

Answer:

<h2>

a. Traditional Cost</h2>

Product 540X

= Revenue - Cost

= 200,000 - 53,000

=$147,000

Product 137Y

= 162,000 - 48,000

= $114,000

Product 249S

= 92,000 - 25,000

= $67,000

<h2>

B. ABC Costing</h2>

Product 540X

= Revenue - Cost

= 200,000 - 47,100

=$152,900

Product 137Y

= 162,000 - 29,000

= $133,000

Product 249S

= 92,000 - 49,900

= $42,100

c.

Difference in Income for 540X

= 4.01%

Difference in Income for 137Y

= 16.67%

Difference in Income for 249S

= -37.16%

Answer: (1) Equilibrium price = 60 and Equilibrium quantity = 120, when I = $1500.

(2) Equilibrium price = 54 and Equilibrium quantity = 108, when I = $1200.

Explanation:

(1) When Average income (I) = $1500

At equilibrium, QD = QS

150 - 3p + 0.1I = 2p

150 - 3p + 0.1 × 1500 = 2p

5p = 300

p =

p = 60

q = 2p ⇒ 2 × 60 = 120

Hence, p and q are equilibrium price and equilibrium quantity, respectively.

(2) If 20% income tax is introduced then Average income (I) = $1500 - 20% of $1500 ⇒ $1500 - $300 = $1200

At equilibrium, QD = QS

150 - 3p + 0.1I = 2p

150 - 3p + 0.1 × 1200 = 2p

5p = 270

p =

p = 54

q = 2p ⇒ 2 × 54 = 108

Hence, p and q are equilibrium price and equilibrium quantity, respectively.