Answer:

li siento no puesobhsdar las resouestav

The great ideas for improving engagement on the website can be tried, EXCEPT Sponsoring a giveaway for a free pair of skis.

Instead of sponsoring a giveaway for a free pair of skis, your e-commerce site should employ integrated marketing.

<h3>What is integrated marketing?</h3>

Integrated marketing involves aligning all marketing tactics with a unified, customer-focused promotional messaging, enabling a consistent customer experience with your sports gear brand.

The advantages of integrated marketing include increasing:

- Brand awareness

- Brand loyalty

- Sales volume and revenue.

Thus, the great ideas for improving engagement on the website can be tried, EXCEPT Sponsoring a giveaway for a free pair of skis.

Learn more about integrated marketing at brainly.com/question/9696745

Answer:

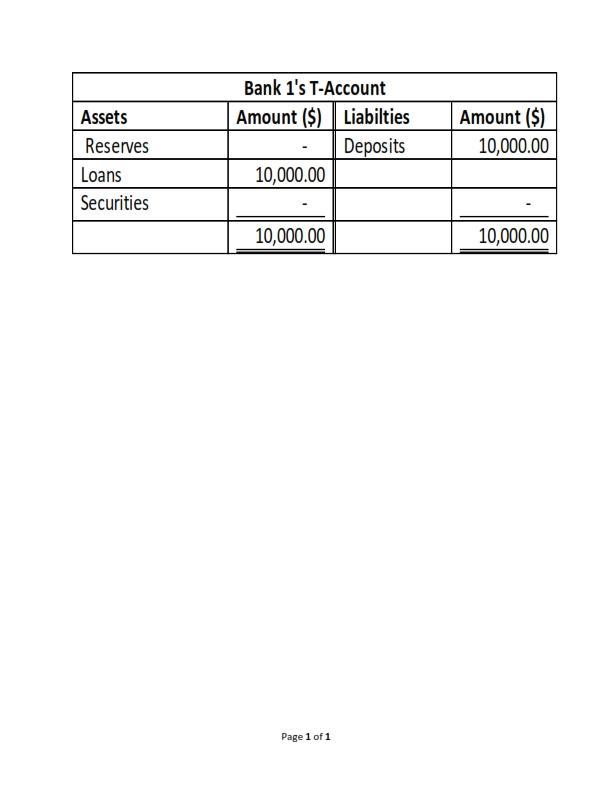

1. Assets is debited for $10,000 as loans.

2. Liabilities is credited for $10,000 as deposits.

Explanation:

Note: This question is not complete as the amount is omitted. The complete question is therefore presented before answering the question as follows:

Suppose banks keep no excess reserves and that all banks are currently meeting the reserve requirement. The Federal Reserve then makes an open market purchase of $10000 from Bank 1.

Use the T-account below to show the result of this transaction for Bank 1, assuming Bank 1 keeps no excess reserves after the transaction.

The explanation of the answer is now given as follows:

Note: See the attached photo for Bank 1's T-Account.

In the attached photo, we can see that:

1. Assets is debited for $10,000 as loans.

2. Liabilities is credited for $10,000 as deposits.