Answer:

$50,120

Explanation:

Account receivable on December 31, 2021 × 3% = 600

Account receivable on December 31, 2021 = $600 ÷ 3% = $20,000

Accounts receivable on January 1, 2021 = $20,000 - $118,000 + $148,000 + $120 = $50,120

Therefore, the balance of accounts receivable on January 1, 2021 is $50,120.

It should be noted that the competitive advantage of Johan's company is being affected by Demand conditions.

<h3>What are Demand conditions?</h3>

Demand conditions can be regarded as the size and nature of the customer base for products, and this usually bring about innovation and product improvement.

This is why Johan was happy that consumers had asked for a better grade of plastic for the toys his company produced.

Learn more about Demand conditions at:

brainly.com/question/4804206

A unilateral contract

With each cup of coffee purchased, the cashier punches a space. The card can be used to redeem a free coffee once all ten spaces have been punched. This serves as an illustration of a unilateral contract.

-Unilateral contract - A unilateral contract explicitly states that payment will only be provided in exchange for performance by one side. A prize or a competition is another illustration of a unilateral contract. In a unilateral contract, the offeror has the right to withdraw it prior to the offeree's commencement of performance. Usually, the revocation must be made in writing. An insurance policy contract, which is typically only partially unilateral, is an illustration of a unilateral contract. The offeror is the sole party having a contractual responsibility in a unilateral contract. Most unilateral agreements are one-sided.

Learn more about the unilateral contract on brainly.com/question/3257527

#SPJ4

Answer:

10%

Explanation:

Cost of kiosk last year = $750

Cost of kiosk this year = $825

Percentage increase = $825-$750 / $750 * 100

Percentage increase = $75 / $750 * 100

Percentage increase = 10%

So the percentage increase in the cost of rent is 10%.

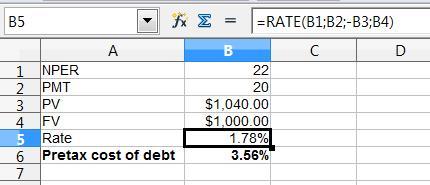

Answer:

a. 3.56%

b. 2.31%

Explanation:

In this question, we use the Rate formula which is shown in the spreadsheet.

The NPER represents the time period.

Given that,

Present value = $1,040

Assuming figure - Future value or Face value = $1,000

PMT = 1,000 × 4% ÷ 2 = $20

NPER = 11 years × 2 = 22 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this,

1. The pretax cost of debt is = 2 × 1.78% = 3.56%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 3.56% × ( 1 - 0.35)

= 2.31%