Answer:

Explanation:

The closing entries for the following accounts are shown below:

1. Service Revenue A/c Dr $44,000

To Income Summary $ 44,000

(Being revenue account closed)

2. Income Statement Dr $33,100

To Depreciation Expense of Equipment $3000

To Salaries Expense $22,000

To Insurance Expense $2,500

To Rent Expense $3,400

To Supplies Expense $2,200

(Being expenses accounts are closed)

3. Income summary A/c Dr $10900

To T. Cruz Capital A/c $10900

(Being the difference is credited to capital account)

4. T. Cruz, Capital A/c Dr $7,000

To T. Cruz, Withdrawals A/c $7,000

(Being withdrawal account is being closed)

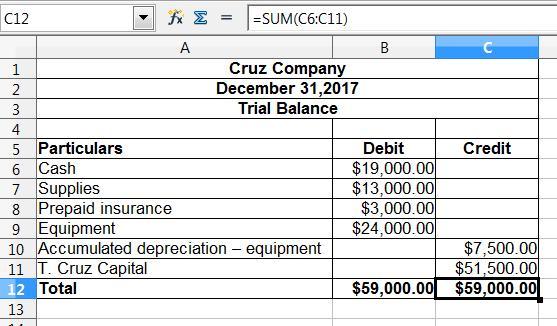

The preparation of the trial balance is presented in the spreadsheet. Kindly find the attachment below: