Answer:

$18,330

Explanation:

For translation of income statement items such net income, the applicable rate is the average rate.

Since the average rate being is $1.41 / Euro, we have:

Value of income in home currency = 13,000 euro * $1.41 = $18,330.

A promotion is the headway of a worker's rank or position in a hierarchical chain of command framework. Advancement might be a representative's reward for good execution. A manager should ensure nondiscrimination in considering a promotion of an employee.

Answer:

Answer for the question:

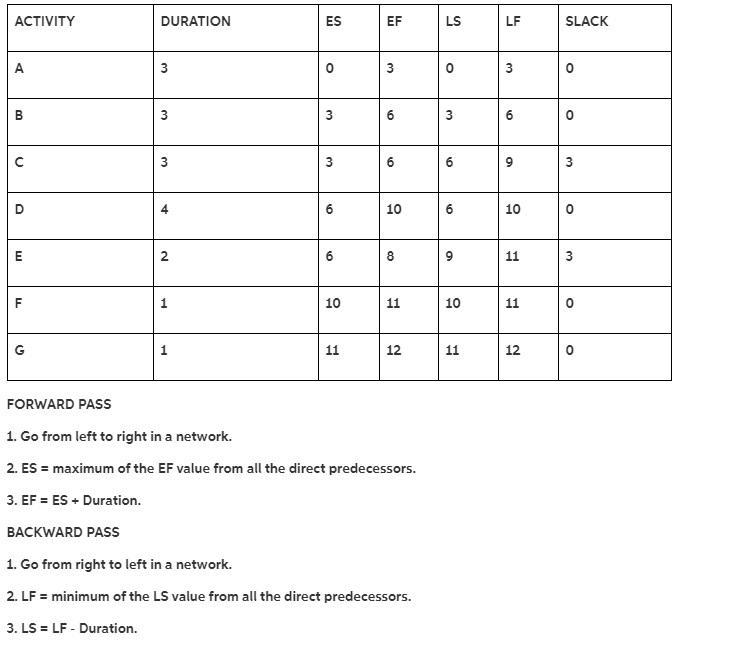

A company must perform a maintenance project consisting of seven activities. The activities, their predecessors, and their respective time estimates are presented below:

Immediate

Activity

Designation

Predecessor

Time in Days

Break down both machines

A

None

3

Clean machine 1

B

A

3

Clean machine 2

C

A

3

Re-set machine 1

D

B

1

Re-set machine 2

E

C

2

Re-calibrate both machines

F

D and E

1

Final test

G

F

2

Using the Single Time Estimate CPM procedure, what is the critical path for the project & the overall project duration?

e. ABCDG & 10 days

c. ABDFG & 10 days

d. ABDFG & 11 days

b. ACEFG & 10 days

a. ACEFG & 11 days

is given in the attachment.

Explanation:

The answer is C households and business

Answer:

d. Finished Goods Inventory

Work In Process Inventory

Explanation:

In the production process when goods raw materials enter into the factory, they are considered as work in process.

On completion from the factory the raw materials that were in work in process are now converted to finished goods.

Inventory is an asset account, and assets is debited when it increases and credited when it reduces.

When all goods have been converted to finished goods there is increase in finished goods inventory, so

1. Debit finished goods inventory

Raw materials in work in process has been converted to finished goods, so the entry for WIP is

2. Credit work in process inventory