Answer: The answer is b -an increase in income will cause the demand curve of an inferior good to shift to the left.

Explanation: An inferior good is a good whose demand reduces as income increases. It's demand has an inverse or negative relationship with income. Therefore as the income of the individual increases, the demand for an inferior good reduces. On a graph, the reduction in demand is depicted by an inward shift of the demand curve or a shift of the demand curve to the left to show a reduction in demand. Income is one of the factors that leads to a shift in the demand curve. The income elasticity would be negative

Shannon should become a journalist writing for a newspaper organisation

The model that requires a manager to assess her own style and her situational control is<u> "Fiedler's contingency model".</u>

The Fiedler Contingency Model was made in the mid-1960s by Fred Fiedler, a researcher who contemplated the identity and qualities of pioneers.

The model expresses that there is nobody best style of initiative. Rather, a pioneer's adequacy depends on the circumstance. This is the aftereffect of two components – "leadership style" and "situational idealness" (later called "situational control").

Answer:

Brand differences are worth promoting if they satisfy following criteria.

*They should be meaningful for the customers. Customers should relate to them.

*Brand differences should be useful from the customer's point of view.

*They should be clearly different from the competitors.

*They should be easily communicable to the customers.

*They should be unique and exciting as well.

*They should be easily memorable too.

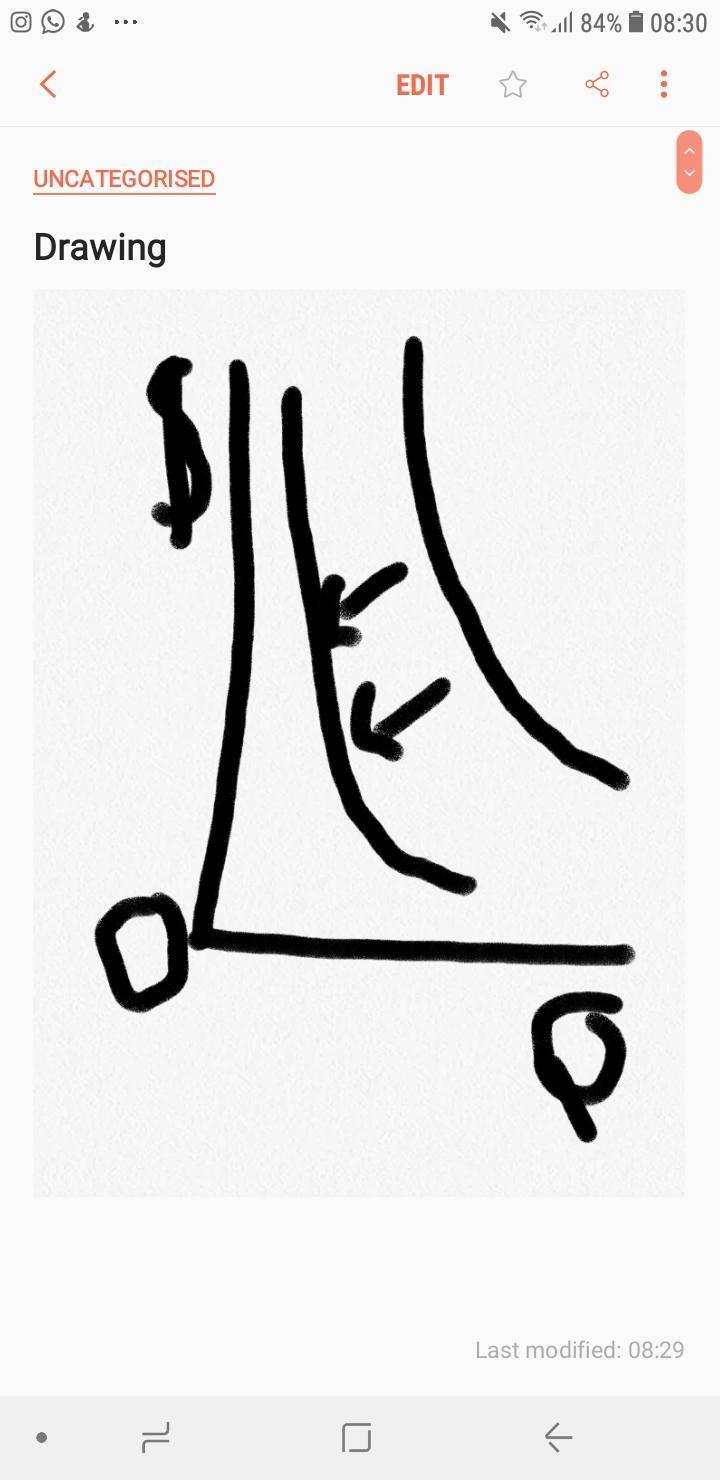

Answer:

The answer is avg cost curve

Explanation:

The long-term result of entry and exit in a perfectly competitive market is that all firms end up selling at the price level determined by the lowest point on the avg cost curve