Answer:

I. It helps users to be better informed, so they can evaluate the risks and returns of different business decisions.

II. It collects and processes data from transactions and events.

III. It organizes financial information into useful reports.

IV. It communicates financial information to decision makers.

Explanation:

Financial accounting is an accounting technique used for analyzing, summarizing and reporting of financial transactions like sales costs, purchase costs, payables and receivables of an organization using standard financial guidelines such as Generally Accepted Accounting Principles (GAAP) and financial accounting standards board (FASB).

The fundamental functions of an accounting system includes;

I. It helps users to be better informed, so they can evaluate the risks and returns of different business decisions.

II. It collects and processes data from transactions and events.

III. It organizes financial information into useful reports.

IV. It communicates financial information to decision makers.

What do you need help with? What's due soon?

Answer:

Using the Put-Call parity principle where the following relationship holds:

Covered Call = Protective Put

Using the above, find the call price:

Call + Strike price / (1 + risk free rate) = Stock price + Put

Call + 18 / (1.08) = 20 + 3.33

Call + 16.67 = 20 + 3.33

Call = 23.33 - 16.67

Call = $6.66

<em></em>

<em>The call option is overvalued at $7 so sell the Call option and buy the Put option and the Stock and borrow $16.67 which is the present value of the Put. </em>

<em>The net gain will be:</em>

<em>= 7 - 6.66</em>

<em>= $0.34</em>

Answer:

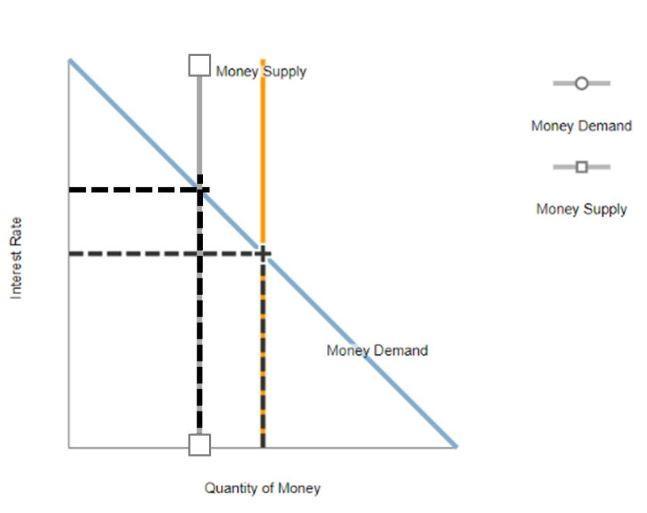

1 and 2: Find attached of the graph

3. The correct answers are:

(a) Price level will fall.

b)The demand for money will fall

Explanation:

(1) A fall in money supply will shift the money supply curve leftward, increasing interest rate and quantity of money. See the first attachment for the graph.

(2) Lower money supply will decrease aggregate demand, shifting AD curve leftward, decreasing both price level and output. See the second attachment for the graph.

(3) The following will happen during transition:

- --(a) Price level will fall.

-- b)The demand for money will fall

These requirements are called Workplace skills. These are

the skills that an employee should possess in order for the company to attain

its goals. These skills are needed of a candidate or an employee and these

skills are needed for all companies or any industry. Examples of workplace

skills are good communication skills, having good analytical skills, good

interpersonal skills, good leadership skills, and being professional.