Answer: Option(d) is correct.

Explanation:

Given that,

Purchases a bond = $10,000

Bond pays at the end of the first, second, and third years = $400

Bond pays upon its maturity at the end of four years = $10,400

(i) Principal amount of this bond = $10,000

It is the issue price of the bond.

(ii) The coupon rate of the bond =

=

= 4% per year

(iii) The term of this bond is 4 years, as it was matured after 4 years.

Answer:

Usher Sports Shop's cash flow from operations for 2018: $5,414,000

Explanation:

Cash at the end of the year = Cash at the beginning of the year + Cash flows from investing activities + Cash flows from financing activities + Cash flows from operating activities

Therefore:

Cash flows from operating activities = Cash at the beginning of the year + Cash flows from investing activities + Cash flows from financing activities - Cash at the end of the year

Cash flows from investing activities of ($2,150,000) <0 and cash flows from financing activities of ($3,219,000) <0.

Cash flows from operating activities = -$980,000 + $2,150,000 + $3,219,000 + $1,025,000 = $5,414,000

Answer:

d. $704,000

Explanation:

The computation of the cash payment for merchandise is shown below:

= Opening balance of accounts payable + purchase made - closing balance of accounts payable

where,

Purchase = Cost of goods sold + closing balance of inventory - opening balance of inventory

= $720,000 + $188,000 - $200,000

= $708,000

The other items values would remain the same

Now put these values to the above formula

So, the value would equal to

= $80,000 + $708,000 - $84,000

= $704,000

The primary concerns when first starting your business are: financing and planning

Answer:

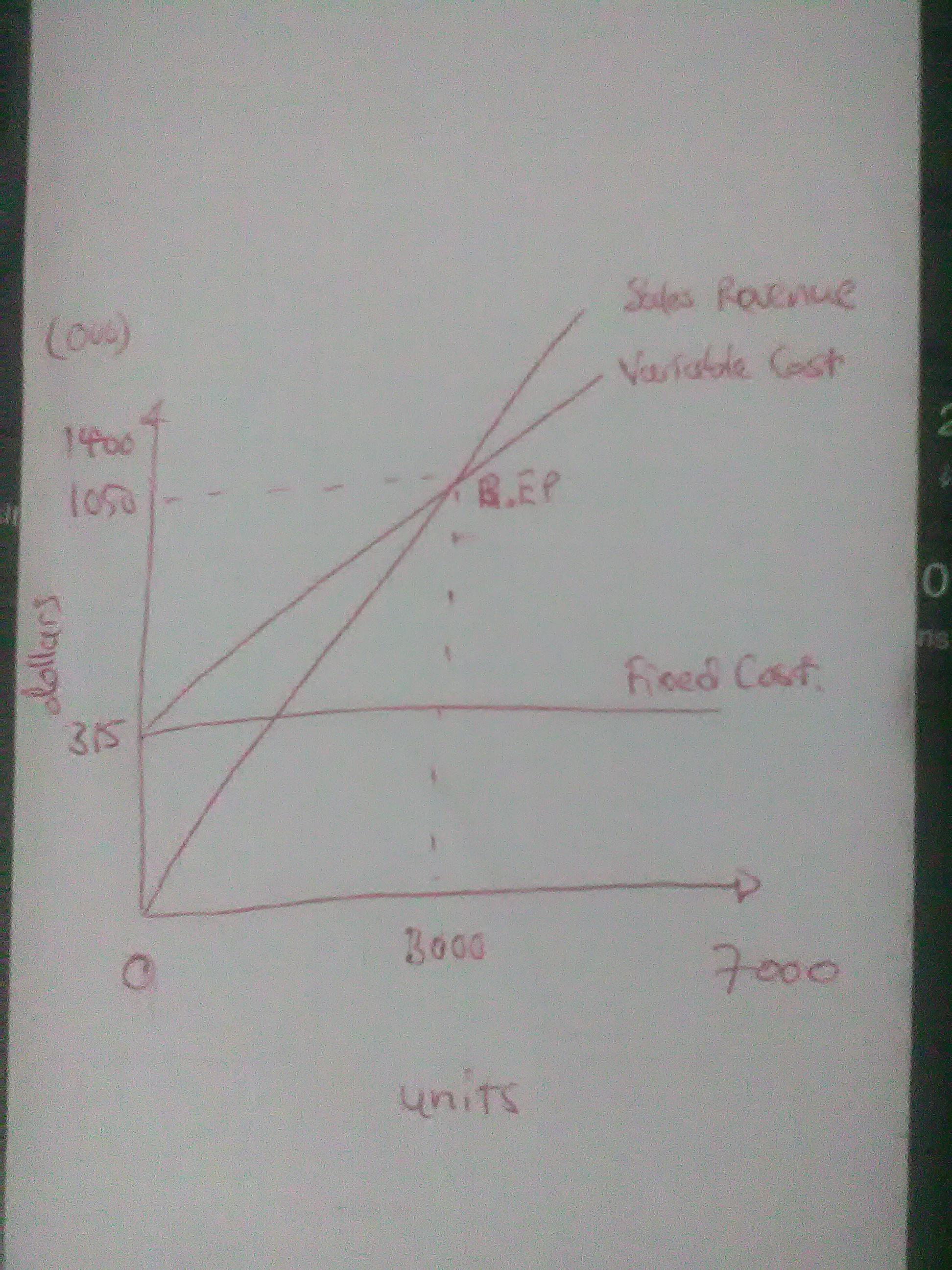

1a. 3,000 units

1b. $1,050,000

2. See attachment.

3. contribution margin income statement

Sales ($350 × 7,000 units) $2,450,000

Less Variable Cost ($245 × 7,000 units)) ($1,715,000)

Contribution $735,000

Less Fixed Costs ( $315,000)

Operating Profit $420,000

Explanation:

Break-even point (sales units ) = Fixed Cost ÷ Contribution per unit

= $315,000 ÷ ($350 - $245)

= 3,000

Break-even point (sales dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $315,000 ÷ ($105/$350)

= $1,050,000