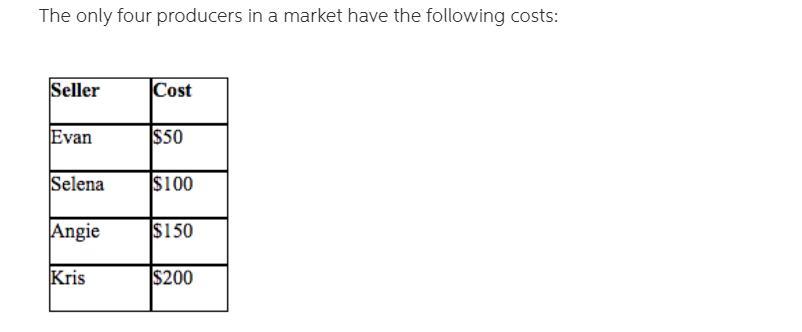

Answer:

$50 or slightly less

Explanation:

If we assume that there is four persons namely E, S, A and K

The producer surplus is the surplus that shows the difference between the seller value and the seller cost

In the case when the seller bid against each other so here the producer surplus would be $100 or slightly less

Here only one person could able to send the good i.e. person E As the cost to the person would be lowered by the goods value

Therefore the option B is correct

Answer:

$2

Explanation:

The computation is shown below:

As we know that

Net realizable value = Selling price − Cost of completion

= $

60 - $10

= $50

And, the cost of the item M-23 is $52

So, the write down of inventory value of the item M-23 is

= Cost of the item - net realizable value

= $52 - $50

= $2

We simply deduct the cost from the net realizable value so that the write down value could come

A The lender may refuse the mortgage.

Answer: D) sampling bias.

Explanation:

Sampling bias refers to a scenario where conditions in the research give more subjects in the population of interest the chance to appear either more or less times than others instead of all the subjects having an equal chance of representation.

The students were to come in at different times yet Graham gave them all the same treatment conditions. This could lead to sampling bias because those who volunteered earlier are likely different from those who volunteered later.

Last year, rosa spent $130,000 on merchandise she sold. she had net sales of $200,000 and expenses of $40,000', therefore rosa’s net profit is <u>$30,000.</u>

<u />

Merchandising is any practice that contributes to the sale of products to retail consumers. At the retail level, merchandising refers to the presentation of products that are sold in creative ways that induce customers to purchase more items or products.

Visual display merchandising in retail means using product design, selection, packaging, pricing, and presentation to sell products and encourage consumers to buy more.

To do. This includes disciplining and discounting the physical presentation of products and displays and deciding which products to present to which customers and when. In retail, creatively linking related products and accessories is often a great way to encourage consumer purchases.

learn more about merchandise here; brainly.com/question/25745683

#SPJ4