Answer:

Task a:

Deferred tax asset = $40,800,000

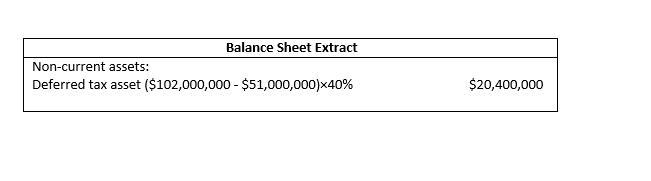

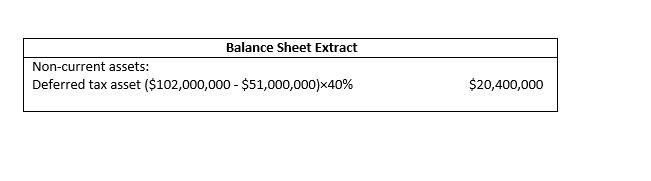

Deferred tax liability = $20,400,000

Task b:

Indicate how the deferred taxes computed in (a) are to be reported on the balance sheet.

Note: Please see the attachments for the balance sheet*

Task c:

Assuming that the only deferred tax account at the beginning of 2017 was a deferred tax liability of $10,000,000, draft the income tax expense portion of the income statement for 2017, beginning with the line "Income before income taxes."

Please see the attachments for the Income statement*

Explanation:

<h2><u>

Task a:</u></h2>

Determine the deferred taxes to be reported at the end of 2017.

<u>Deferred tax asset</u>

Deferred tax asset = $102,000,000 × 40%

Deferred tax asset = $40,800,000 (answer)

<u>Deferred tax liability</u>

Deferred tax liability = $51,000,000 × 40%

Deferred tax liability = $20,400,000 (answer)

<h2><u>

Task b:</u></h2>

Indicate how the deferred taxes computed in (a) are to be reported on the balance sheet.

<h2><u>

Explanation:</u></h2>

<u>Deferred tax asset</u>

- When <u>income tax expense is smaller than income tax payable</u> as a result of deducting any <u>non-cash expenses</u> in accounting books, some income tax expense is deferred to the future.

- The<u> larger</u> income tax payable on tax returns creates a <u>deferred tax asset</u>, which companies can use to pay for deferred income tax expense in the future.

- Deferred tax assets may be presented as <u>current assets</u> if a temporary difference between <u>accounting income</u> and <u>taxable income</u> is reconciled the following year.

<u>Deferred tax liability</u>

- When<u> income tax expense is greater than income tax payable</u> as a result of no recognition of any noncash revenues in tax returns, some income payable is deferred to the future.

- The <u>smaller</u> income tax payable on tax returns creates a <u>deferred tax liability</u>, which companies must meet by paying any deferred income tax payable in the future.

- Deferred liabilities may be presented as <u>current liabilities</u> if a temporary difference between accounting income and taxable income is reconciled the following year.

Note: <u>The balance sheet extract is attached:</u>

<u></u>

<h2><u>

Task c:</u></h2>

Assuming that the only deferred tax account at the beginning of 2017 was a deferred tax liability of $10,000,000, draft the income tax expense portion of the income statement for 2017, beginning with the line "Income before income taxes."

Note: <u>The income statement extract is attached:</u>

Note: <u>The relevant working also attached</u>

<u></u>