Answer:

A. The first scenario where all three workers spend all their time mowing lawns,

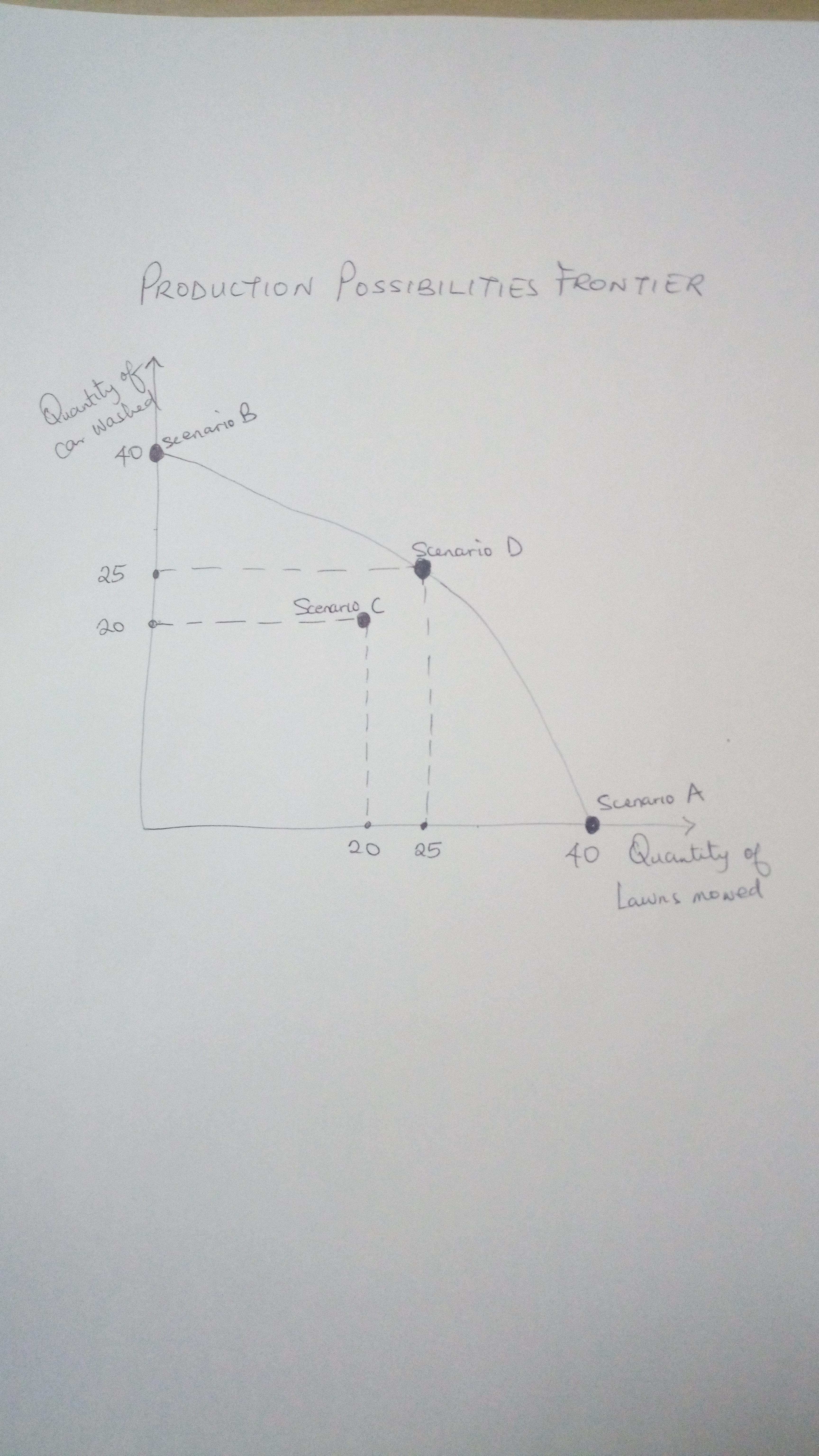

In 10 hours = Larry mows 10 lawns, Moe mows 10 lawns, and Curly mows 20 lawns = (<em>Total is 40 lawns mowed, and 0 cars washed</em>)

B. The second scenario where all three workers spend all their time washing cars

In 10 hours = Larry washes 10 cars, Moe washes 20 cars, and Curly washes 10 cars = (<em>Total is 40 cars washed, and 0 lawn mowed</em>)

C. The third scenario where all three workers spend half their time on each activity then;

In 5 hours for mowing lawns and 5 hours for washing cars we get:

Larry mows 5 lawns and washes 5 cars

Moe mows 5 lawns and washes 10 cars

Curly mows 10 lawns and washes 5 cars

<em>In total they mowed 20 lawns and washed 20 cars</em>

D. The fourth scenario, Larry spends half his time on each activity, while Moe only washes cars and Curly only mows lawns.

Larry mows 5 lawns and washes 5 cars

Mow washes 20 cars

Curly mow 20 lawns

<em>In total, 25 lawns will be mowed and 25 cars will be washed</em>

When this is plotted, the production frontier would produce a bow out shape, which is as a result of opportunity cost.

From the diagram, it can be clearly seen that Scenario C is inefficient because it is possible to mow more lawns and also wash more cars without actually reducing the production of others to 25 each.

Yes C is inefficient because more lawns can be mowed and more cars can be washed by simply just reallocating time of the 3 workers.

Explanation: