Answer:

the depreciation that should be charged over the useful life each year is $20,000

Explanation:

The computation of the depreciation expense using the straight line method is shown below:

= (Purchase cost of an equipment - residual value) ÷ (useful life)

= ($135,000 - $15,000) ÷ 6 years

= $120,000 ÷ 6 years

= $20,000

hence, the depreciation that should be charged over the useful life each year is $20,000

Answer:

the ending inventory using the FIFO cost flow assumption is $282,900

Explanation:

The computation of the ending inventory using the FIFO cost flow assumption is shown below;

But before that first we have to determine the ending inventory units i.e.

= 280 + 380 + 480 + 290 - 1,200

= 230 units

So, the ending inventory is

= 230 units × $1,230

= $282,900

Hence, the ending inventory using the FIFO cost flow assumption is $282,900

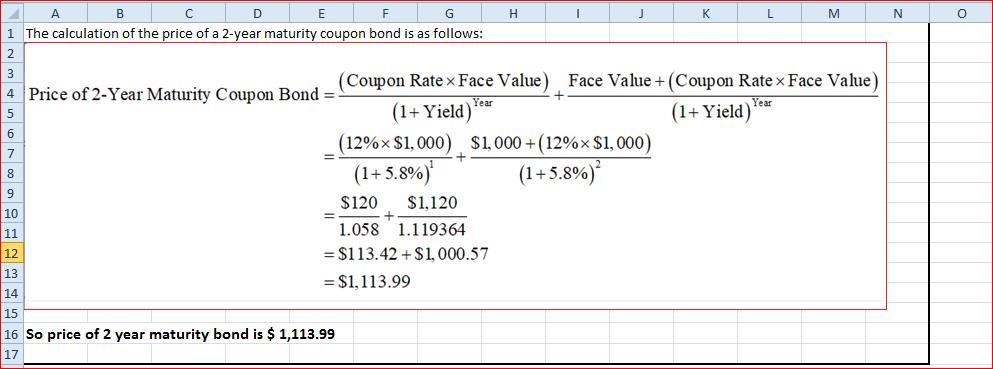

Answer:

<em>$111.11 or 111.11% of face value</em>

Explanation:

Assuming the face value of $100 for all bonds (without loss of generality)

If the two year coupon bond is repackaged as a one year zero coupon bond paying $12 after one year and another two year bond paying $112 after 2 years, the price of the two zero coupon bonds are given as

Price of one year Zero coupon bond = 12/1.05 = $11.43 (one year ZCB has YTM of 5%)

Price of two year Zero coupon bond = 112/1.06^2 = $99.68 (two year ZCB has YTM of 6%)

So, one can sell the repackaged bonds at a price = $11.43+ $99.68 = $111.11 or 111.11% of face value

The type of marketing that this is is called business to customer strategy. This is called B2C marketing.

<h3> </h3><h3>What is a business to customer strategy?

</h3>

This is a type of marketing strategy that has to do with the approach that businesses take to sell their goods and their services to the customers that they have.

The business here is utilizing the fact that they game is at the half time to sell their goods.

At this time, a lot of the audience would feel the need to be refreshed and would need something to eat

Read more on business to customer strategy here:

brainly.com/question/24803497

Answer:

The correct answer is A. Implement single sign-on.

Explanation:

The single sign-on (SSO), is the working method by which workers gain access to different business applications through a registration procedure. For example, when you log in from your computer, you connect directly to all the computer software. There are two ways of single sign-on:

- Basic SSO

- Federated SSO

With the basic SSO, the password is saved in a "vault", a type of virtual security. This storage usually occurs in the cloud. Then, that vault password is retrieved for all applications that must log in later.

Federated SSO is a more advanced form of single sign-on. In this case, the password data is not stored or transmitted. First, they become tokens. Therefore, another code is created and the original password is not known by any other system.