Answer:

$1,333,333.33

Explanation:

Exchange rates (Ps/$)3.50 4.50

New exchange rate (Ps/$)6.00

Less Exchange rate allowable (Ps/$)4.50

= (Ps/$)1.50

Shares of De Magistris' 0.75

Shares of Acuña's..0.75

Top of range 4.50

Add Share 0.75

=5.25

Let Assumed hat 6 months of imports will still be (Ps) $7,000,000

÷ Exchange rate for DeMagistris (Ps/$)5.25

= $1,333,333.33

<u><em>Explanation</em></u>:

<u>Question 1.</u> These options apply;

- Create a culture of innovation by inviting and expecting employees to contribute new ideas.

- Hire people with new skills and perspectives and train current employees on new skills.

- Restructure the organization to be more customer-centric and make work processes more efficient.

<u>Question 2.</u> These options apply;

- Think about new possibilities for the organization.

- Spend a good deal of time determining what the problem is and find out what caused it.

- Create deadlines and checkpoints for solving the problem

<u>Question 3</u>

B. slow moving and stable

<u>Question 4</u>

D. incremental

<u>Question 5. </u>

D. made a proactive change

Answer:

Total net activity in the inventory account in February was:

D : $97,216.

Explanation:

Purchases________________________ 100000

FOB_____________________________ 200

Allowance_______________________ 1000

Debt____________________________ 99200

terms 2/10 n/30___________________ 2%

1984

Net activity in the inventory_________ 97216

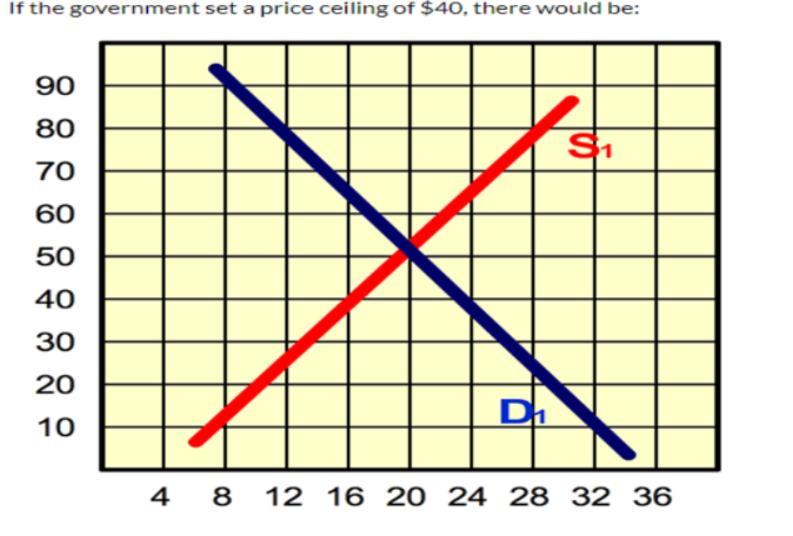

Answer:

A surplus (or excess demand) of about 8 units

Explanation:

The picture attached shows the diagram necessary for the question which is part of the question. Solution is given below;

At the above ceiling at price of 40$

Quantity supplied will be 16

Quantity demanded will be 24

So when demand is more than supply than there will be a shortage in quantity by (24-16) 8 units.

When there is demand more than supply than it is an excess demand.

So surplus or excess demand by 8 units.

Answer:

Option B is the correct answer

Explanation:

Option B is correct because the yield on a 5-year bond must exceed that on a 2-year Treasury bond for the following reasons.

Firstly, after two years, the expected rate of inflation will be constant after two years.

Secondly, there is also a maturity risk premium that increases with increase in the maturity of the board.

These are the two reasons why the yield on a 5 year treasury bond must exceed on a 2 year treasury bond