Answer:

D.

an income tax rate cut

Explanation:

Fiscal stimulus programs are government policies aimed at accelerating growth in times of recessions. The government adjusts its spending or tax rates to influence the economy's direction. A stimulus is meant to increase output and increase income.

An income tax rate cut increases the amount of disposable income of consumers. An increase in disposable incomes boosts consumer spending, which results in increased demand. Firms in the service and manufacturing industries will respond to the rise in demand by increasing production. A rise in output creates employment opportunities.

Answer:

<u>Sales Budget</u>

January February March April May

Units Sold 200 300 400 300 400

Price per unit $10 $ 10 $ 10 $ 10 $ 10

Sales Rev $ 2.000 $ 3.000 $ 4.000 $ 3.000 $ 4.000

Explanation:

We have to multiplithe amount of units sold each month by the sales price per unit of each month.

For the second question, which is the production budget we require the beginning inventory at Jan 1st and the desired inventory policy else, we cannot complete it. Please add this as details for the question Thank you =)

Answer:

The answer is letter D.

Explanation:

A partner withdraws from a partnership by selling her interest to another person who currently is not associated with the firm. As a result of this transaction, the capital account balance of the other partners in the partnership wil remain the same.

Answer:

Form Utility

Explanation:

Form Utility represents the value of a finished product as perceived or seen by the consumer of the product. Form utility actually describes the attractiveness of a product seen by a customer. This attractiveness is as a result of a manufacturer's ability to take a raw material (which is not too useful to the consumer) and transform it to a finished and desirable product for the consumer.

A consumer percieves or sees a product more useful in its consumption or finished form rather than its raw state.

A dress manufacturer takes the silk, thread and zippers as raw materials and transform them into an attractive bridesmaid gown for the consumer, this is form utility.

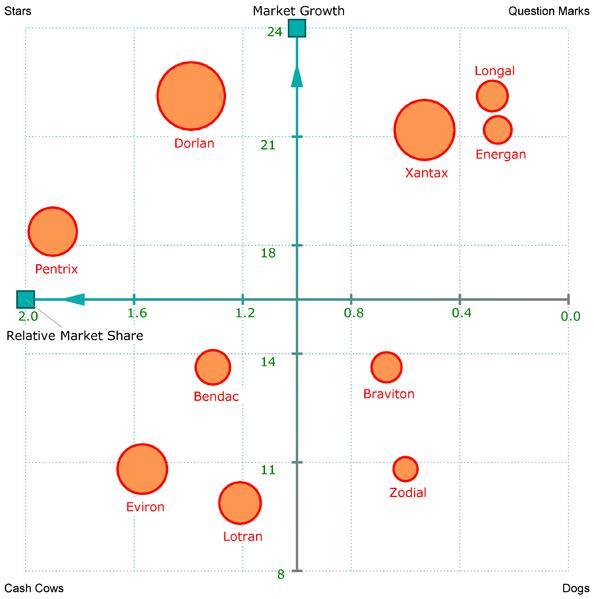

The Cash cows under the BCG Matrix are businesses, assets, and or products that have a consistent cash flow, high market share and low market growth.

<h3>What is the BCG Matrix?</h3>

The BCG Matrix is a strategic analysis tool that was developed by Boston Consulting Group which highlights and compares various kinds of business and or products.

Other sections of the matrix are:

- Stars (Upper Left Corner)

- Cash Cows (Lower Left Corner)

- Question Marks (Upper Right Corner) and

- Dogs (Lower Right Corner)

The correct answer, thus, is A: Slow Industry Growth but Strong Market Share Position, which as explained can be due to high cashflows.

See the link below for more about BCG Matrix:

brainly.com/question/24515909