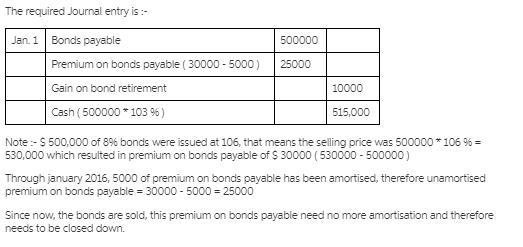

Answer:

Multiply the amount in the account by the nominal interest rate

Explanation:

Answer:

1

Explanation:

A perfect competition is characterized by many buyers and sellers of homogenous goods and services. Market prices are set by the forces of demand and supply. There are no barriers to entry or exit of firms into the industry.

In the long run, firms earn zero economic profit. If in the short run firms are earning economic profit, in the long run firms would enter into the industry. This would drive economic profit to zero.

Also, if in the short run, firms are earning economic loss, in the long run, firms would exit the industry until economic profit falls to zero.

In a perfect monopoly, there is only one firm operating in the industry

In a monopolistic competition, differentiated products are sold

In an oligopoly, there are few large firms

Answer:

Assortment warehousing is a form of warehousing that combines classic operations with light manufacturing and packaging duties in order to assure short customer lead times.

Explanation:

Warehousing

This have different points of view. The traditional view about warehousing is that it is a place used in for storage or holding of goods/ inventory

The contemporary opinion about warehousing is that it is has function set in place to mix inventory assortments to meet the need of customer. It deals with the storage of products which is held to a minimum.

Warehousing types

This includes;

1. Distribution centers

2. Consolidated terminals

3. Break-bulk facilities

4. Cross-dockers

assortment warehousing

This is a known form of warehousing. It consists of when different type of goods is held close to the source of demand in order to assure short customer lead time.

Answer:

Answer: Yes, There is a linear correlation between the weights of the bears and their chest sizes because the absolute value of the test statistics 0.961 exceeds the critical value

Explanation:

Claim: There is a linear correlation between the weights of the bears and their chest sizes

Null hypothesis, H₀ : p=0 (there is no significant correlation)

Alternative hypothesis, H₁ : p ≠0 (there is no significant correlation)

Level of significance, α = 0.05

Decision rule: Reject H₀ if robserved ≥ rcritical

Sample correlation coefficient r = robserved = 0.961

Yes, There is a linear correlation between the weights of the bears and their chest sizes because the absolute value of the test statistics 0.961 exceeds the critical value