Answer:

b. greater than face value

Explanation:

To find out the how much is selling amount, first we have to do the calculations which are shown below

The computation of the value of the bond is shown below:

= Present value of interest + Present value of full and final payment

where,

In semi annually, the rate of interest is divided by 2 and the time period is double

Present value of interest equals to

= $10,000 × 12% × 8.5136

= $10,216.32

The 7.36009 is a PVAF Refer to the PVAF table

And, the Present value of maturity equals to

= $10,000 × 0.1486

= $1,486

The Present value factor is computed below:

= 1÷( 1 + rate)^time

=1÷(1 + 0.10)^20

Now put these values to the above formula

So, the value would equal to

= $10,216.32 + $1,486

= $11702.32 approx

Answer:

a) In compliance with the IFRS

Explanation:

Since in the question it is mentioned that The financial statement of kansas ltd would be authorized by the management and auditors as on Feb 15 fpr issuance. On Feb 20 it settled as a plaintiff a 5 million euro lawsuit. Now the CFO of the company have make the second decision regarding the financial statement presentation in which he decides not to record this settlement so here is in compliance with the IFRS

Therefore the option A is correct

Answer:

$0.10 is the correct answer.

Explanation:

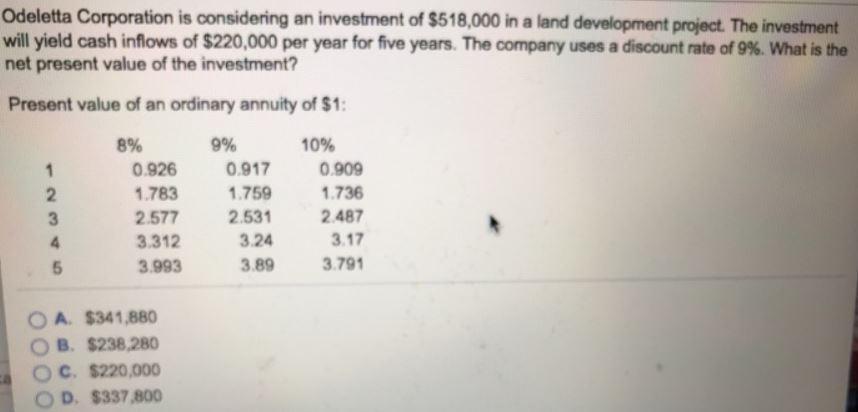

Answer: $337,800

Explanation:

Cashflow is constant so is an annuity.

The Present value of the Investment;

= Present Value of Cashflow - Investment cost

= (220,000 * Present value interest factor of an annuity, 5 years, 9% ) - 518,000

= (220,000 * 3.89) - 518,000

= 855,800 - 518,000

= $337,800