<span>If you have questions about taxes, the best place to get answers would be your local tax professional. Use the internet to read reviews about local professionals and decide which one would be the best fit for your needs.</span>

Answer:

Explanation:

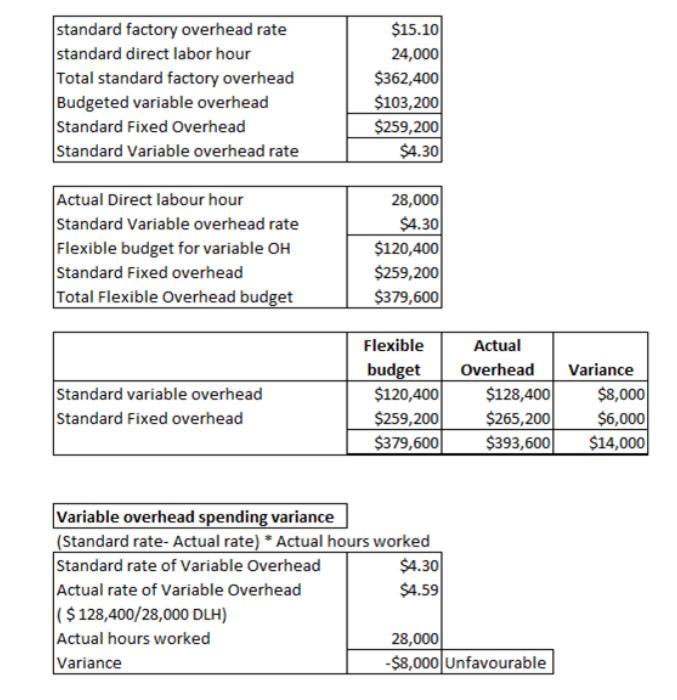

check attached file for solution

The Mute's margin of safety (MOS) in sales dollars is: d. $54,290,602.

<h3>Margin of safety</h3>

First step

Breakeven=$12,143,500/( $3,350-$1,480)/$3,350

Breakeven=$12,143,500/$1870/$3370

Breakeven=$12,143,500/0.5548961424332

Breakeven=$21,884,275

Second step

Margin of safety:

Margin of safety=(22,700×$3350)-$21,884,275

Margin of safety=$54,290,602

The correct option is D.

Learn more about Margin of safety here:brainly.com/question/9797559

#SPJ1

Answer:

Privacy

Explanation:

The law gives right to every person to their own privacy i.e. for one to live without being subjected to unwarranted and undesired publicity. The right to privacy actively deals with issue surrounding the personal matters of an individual and the right for them to be let alone.

A violation of this right is called the tort of invasion of the right to privacy. The tort of invasion of the right to privacy occurs when an individual sues another person who he/she believes has trespassed on his right to privacy. This trespass might come in form of disclose of their private information, or using the person`s name and associated things for another person`s gain without their consent.

Answer: Ethical Obligations and Decision-Making in Accounting-The Heading is devoted to helping students cultivate the ethical commitment needed to ensure that their work meets the highest standards of integrity, independence, and objectivity.

* This program is designed to provide instructors with the flexibility and pedagogical effectiveness, and includes numerous features designed to make both learning and teaching easier.

Explanation: The first, addressed in Part I, is the administrative cost of deregulation, which has grown substantially under the Telecommunications Act of 1996.Part II addresses the consequences of the FCC's use of a competitor-welfare standard when formulating its policies for local competition, rather than a consumer-welfare standard. I evaluate the reported features of the FCC's decision in its Triennial Review. Press releases and statements concerning that decision suggest that the FCC may have finally embraced a consumer-welfare approach to mandatory unbundling at TELRIC prices. The haphazard administrative process surrounding the FCC's decision, however, increases the likelihood of reversal on appeal.Beginning in Part III, I address at greater length the WorldCom fraud and bankruptcy. I offer an early assessment of the harm to the telecommunications industry from WorldCom's fraud and bankruptcy. I explain how WorldCom's misconduct caused collateral damage to other telecommunications firms, government, workers, and the capital markets. WorldCom's false Internet traffic reports and accounting fraud encouraged overinvestment in long-distance capacity and Internet backbone capacity. Because Internet traffic data are proprietary and WorldCom dominated Internet backbone services, and because WorldCom was subject to regulatory oversight, it was reasonable for rival carriers to believe WorldCom's misrepresentation of Internet traffic growth. Event study analysis suggests that the harm to rival carriers and telecommunications equipment manufacturers from WorldCom's restatement of earnings was $7.8 billion. WorldCom's false or fraudulent statements also supplied state and federal governments with incorrect information essential to the formulation of telecommunication policy. State and federal governments, courts, and regulatory commissions would thus be justified in applying extreme skepticism to future representations made by WorldCom.Part IV explains how WorldCom's fraud and bankruptcy may have been intended to harm competition, and in the future may do so, by inducing exit (or forfeiture of market share) by the company's rivals. WorldCom repeatedly deceived investors, competitors, and regulators with false statements about its Internet traffic projections and financial performance. At a minimum, WorldCom's fraudulent or false