I think the answer is what and for whom.

In order to produce deals, there are 2 components need to be considered by every companies. The suitable product to sell (which answer the 'what' part of the economic question) and other parties that are willing to buy the product that they sell (which answer the 'for whom' part of the economic question)

They are called (legacy) systems

(Brainliest please)

Answer:

This situation would cause a 2015 deferred tax amount of $900

Explanation:

Deferred tax liability: It is a liability which shows a difference between taxable income and the accounting earnings available before taxes.

In mathematically,

Deferred tax liability = Taxable income - accounting earnings available before taxes

In this question, we multiply the revenue item by an income tax rate

In mathematically,

= Revenue item × income tax rate

= $3,000 × 30%

= $900

Hence, this situation would cause a 2015 deferred tax amount of $900

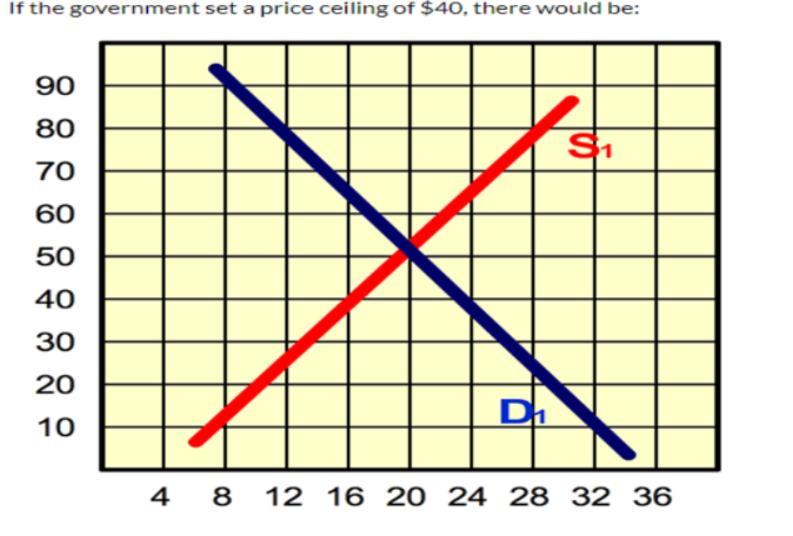

Answer:

A surplus (or excess demand) of about 8 units

Explanation:

The picture attached shows the diagram necessary for the question which is part of the question. Solution is given below;

At the above ceiling at price of 40$

Quantity supplied will be 16

Quantity demanded will be 24

So when demand is more than supply than there will be a shortage in quantity by (24-16) 8 units.

When there is demand more than supply than it is an excess demand.

So surplus or excess demand by 8 units.

Your answer to this question is increased by $1000