Answer: A - nominal wages are slow to adjust to changing economic conditions

Explanation:

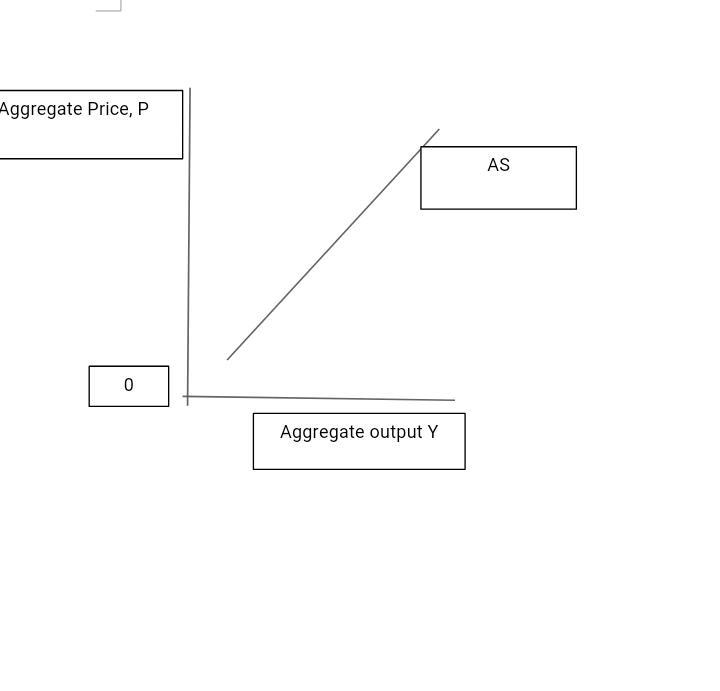

In the short run, the costs of many of the factors used in the production process are fixed. For example labours wage is fixed for a number of years because of labour contracts. Also the raw materials used in the production process have long term agreements that fix their prices.

As a result of factors of production been fixed in the short run, when general price level rises and the cost of production remains constant, profit also rises.

Firms take advantage of this rise in price and increase production and the quantity of aggregate supply increases. This is why the short run aggregate supply curve is upward sloping.

Advertising is a paid form of communication, delivered through media from an identifiable source, about a service, product and Idea.

<h3>What is advertising as a form of communication?</h3>

A product or service's customers can be reached through advertising. According to the Advertising Association of the UK, advertisements are messages that are paid for by those who send them and are meant to inform or persuade individuals who receive them.

The advertising industry is made up of businesses that advertise, agencies that produce the ads, media that run the ads, and a large number of individuals who take the ads all the way to the consumer or recipient, including copy editors, visualizers, brand managers, researchers, creative minds, and designers.

Learn more about advertising, here:

brainly.com/question/3163475

#SPJ1

Answer:

Explanation:

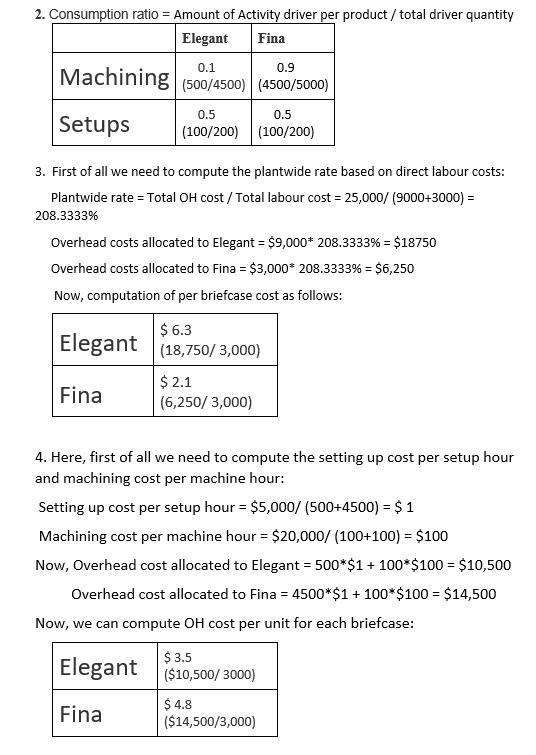

1. Yes, these costs are accurately traced to each briefcase. Because these are variable cost and incurred upon per unit as per the product requirement and specification.

Check attachment for 2, 3 and 4.

For 3b. please provide the statements which are to checked.

As the drug industry in Canada grow, Drugs that usually could be obtained only through criminal organization now can be easily obtained over the counter (as long as the requirements are met)

This make many major criminal organizations to lose their power and profits from their operation in Canada

As long as they have <span>long arm statutes.

</span>