Answer:

Second National Bank

Present value (PV) = $5,400

Future value (FV) = $13,900

Interest rate (r) = 10% = 0.10

FV = PV(1 + r)n

$13,900 = $5,400(1 + 0.10)n

<u>$13,900</u> = (1.10)n

$5,400

2.574074074 = (1.10)n

Log 2.574074074 = n log 1.10

<u>Log 2.574074074</u> = n

Log 1.10

n = 9.9 years

None of the answers is correct

Explanation:

In this case, we will apply the formula of future value of a lump sum. The present value, interest rate and future value were provided with the exception of number of years. Thus, the number of years becomes the subject of the formula. The future value equals present value, multiplied by 1 plus interest rate, raised to power number of years.

Answer:

Firm A will buy all of the firm B's pollution permits. Each one will cost between $100 and $200.

Explanation:

The firm B will gain from the trade of pollution permits. Firm A will need higher pollution permits since it emits 100 tons of chemicals into air and the cost for eliminating each ton is $200. This cost is higher than the cost to Firm B which is $100 only. Firm A will buy all the pollution permits from Firm B and there will advantage for the Firm B to gain from the trade.

Answer:

B

Explanation:

If investors do not have adequate information about the company they are investing, they would demand an higher rate of return. This would increase the cost of raising capital. So, financial managers who want to raise capital at a cheap rate would have the incentive to disclose information

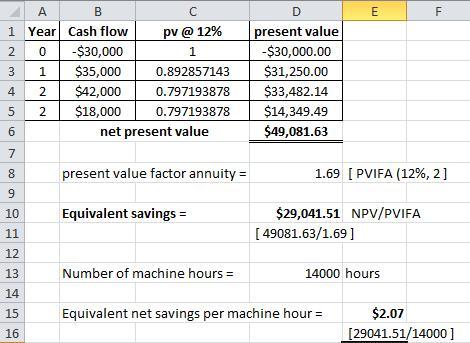

Answer:

$2.07

Explanation:

the complete answer details is found in the attachment below

Answer: All of these choices are correct.

Explanation:

You didn't give the options to the question. The options include:

testing costs prior to placing the equipment into production

transportation costs

installation costs

All of these choices are correct.

Acquisition cost, is the total cost that is recognized by a company on its books for the purchase of an asset. These costs include the transportation cost, installation cost, shipping cost, testing costs, sales taxes, customs fees, etc.

Therefore, based on the explanation, the correct option is All of the choices are correct.