Here is the full question.

The employee credit union at State University is planning the allocation of funds for the coming year. The credit union makes four types of loans to its members. In addition, the credit union invests in risk-free securities to stabilize income. The various revenue producing investments together with annual rates of return are as follows:

Type of Loan/Investment Annual Rate of Return (%)

Automobile loans 8

Furniture loans 10

Other secured loans 11

Signature loans 12

Risk-free securities 9

The credit union will have $1.6 million available for investment during the coming year. State laws and credit union policies impose the following restrictions on the composition of the loans and investments.

Risk-free securities may not exceed 30% of the total funds available for investment.

Signature loans may not exceed 10% of the funds invested in all loans (automobile, furniture, other secured, and signature loans).

Furniture loans plus other secured loans may not exceed the automobile loans.

Other secured loans plus signature loans may not exceed the funds invested in risk-free securities.

How should the $1.6 million be allocated to each of the loan/investment alternatives to maximize total annual return? Round your answers to the nearest dollar.

Automobile Loans $

Furniture Loans $

Other Secured Loans $

Signature Loans $

Risk Free Loans $

What is the projected total annual return? Round your answer to the nearest dollar.

$

Answer:

Explanation:

Let the amount invested in:

Automobile loans be Xa,

Furniture Loans be Xf,

Other Secured Loans be Xo,

Signature loans be Xs, &;

Risk-free loans be Xr

In reference on the Annual returns rate given;

Total annual returns = 8%×Xa + 10%×Xf + 11%×Xo + 12%×Xs + 9%×Xr

The various constraints given can be written as follows:

Xa + Xf + Xo + Xs + Xr = 1,600,000-----Constraint for amount available for investment

Xr = 30%*1,600,000 ----- Constraint for maximum risk free investment

Xs = 10%*(Xa + Xf + Xo + Xs) ----- Constraint for maximum amount in signature loans

Xf + Xo = Xa ------- Constraint for Furniture and other secured loans

Xo + Xs = Xr ------ Constraint for other secured loans and signature loans

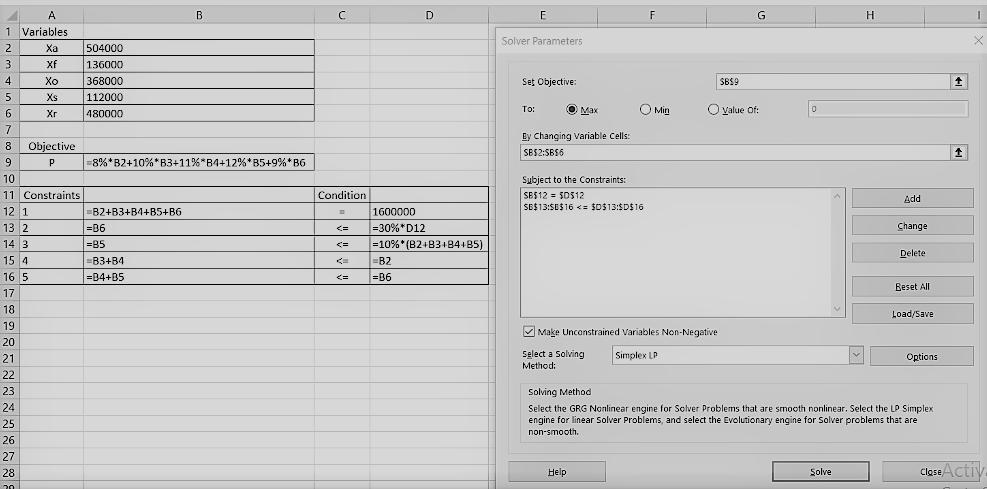

Using the Excel Formula for solving this;

we have the following result.

Automobile Loans $ 504,000

Furniture Loans $ 136,000

Other Secured Loans $ 368,000

Signature Loans $ 112,000

Risk-Free Loans $ 480,000

The projected total annual return = $ 151,040

The computation of the excel formula on how we arrived at those valid figures above is shown in the attached files below.

Thanks!