Answer:

The answer is: $6.50

Explanation:

Assuming you bought the MP3 player in store A, to calculate the finance charge for June we can use the following formula (applicable to daily balance method):

- [(beginning balance + ending balance) / 2] x (annual interest rate / 12)

= [($700 + $600) / 2] x (12% / 12) = ($1300 / 2) x 0.01 = $650 x 0.01

= $6.50

Answer:

$2,538,000

Explanation:

Paid in capital in excess of par-common stocks= $102*94,000-94000*3*25=$2,538,000

The preference shares were valued at $102*94,000 less the amount of common stocks issued at par (94,000*3*25) for conversion of preference stocks to common stocks will give paid in capital in excess of par for common stocks.

The excess amount is also called share premium paid.

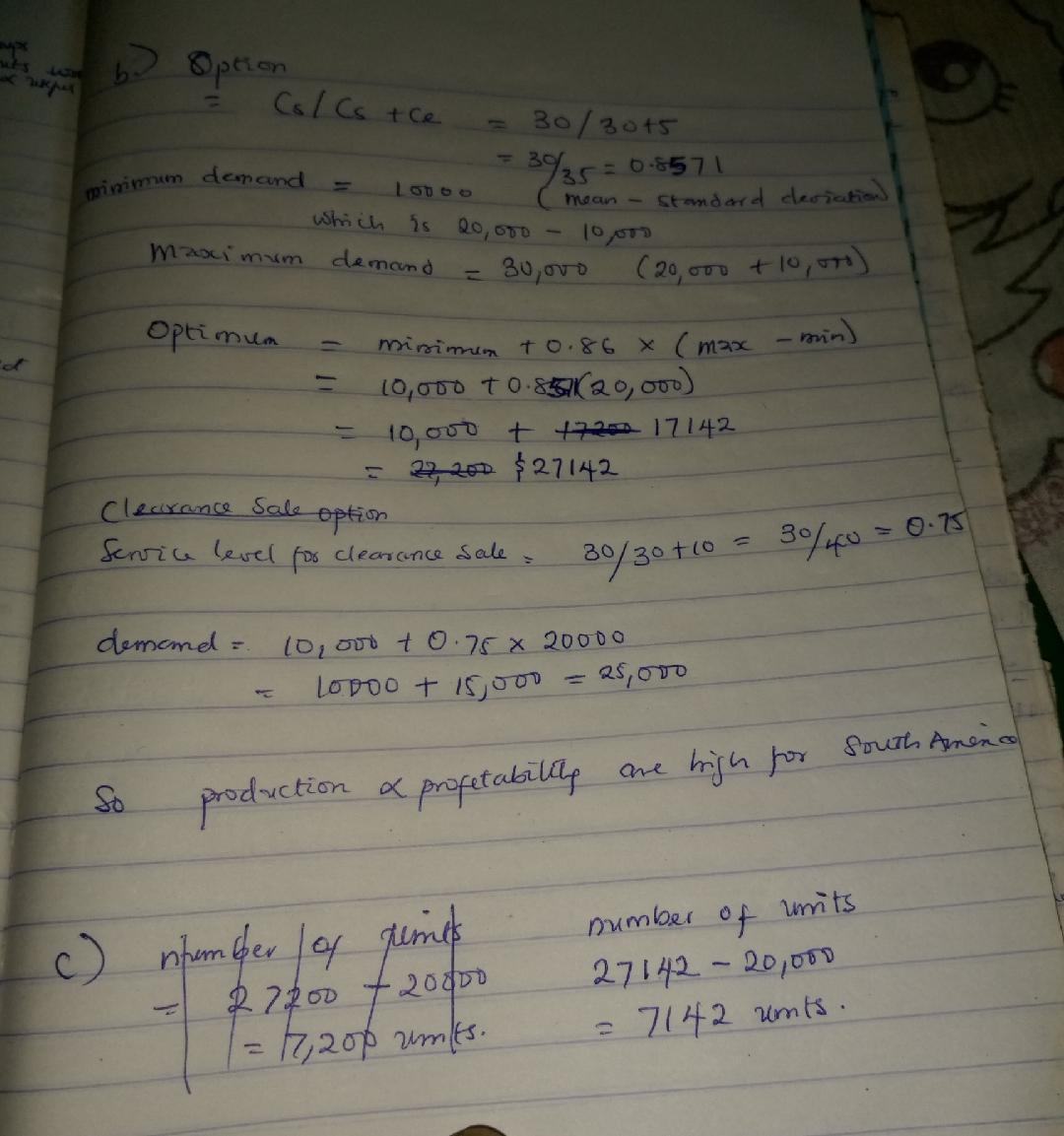

Answer:

The question puts

Mean demand to be 20000

Standard deviation to be 10000

Storage cost = 60-30= 30

Excess cost to be 30+5-25 = 10

For shipping to south america

Excess cost = 30+5+5-35 = 5 dollars

A.

It is of more benefits to ship to south america because we have an excess cost of 5 dollars and excess clearance cost of 10 dollars

B.

Production and profitability are high for south america. Please check attachment for the calculations I added

C.

Number of units

27142-20000

= 7142 units.

The answer is experience, it is because when she works with other companies and to be able to work in different places, she is able to gather and exhibit experiences in which are important to potential employers as this will set as a beneficiary for them.