In my opinion, introductions can be made by a persons background in general, for example, lets say that there is someone that applies for a job at your business and your business gives people their own personal work vehicle and the person applying for the job has many tickets on their record for speeding. I don't think id want someone like that working for me, nonetheless, when it comes to cultural background as into worshiping any sort of religion, as long as it doesn't interfere with work relations, Id say...

<u>True </u> Introductions should be conducted the same way regardless on someones cultural background.

NPV stands for net present value, which refers to the amount of money that is invested today and how much it could potentially be worth in the future. If Alby Ldt. decided they did not want to invest after calculating the potential NPV, it's likely that the future value of the purchase would not be worth the investment.

Answer:

b. $ 240,000

Explanation:

Calculation for what Kat should recognize as compensation expenses

Using this formula

Compensation expenses= (Purchase shares ×Value of options)/ Years of Service

Let plug in the formula

Compensation expenses=(60,000 shares

x $8 per option) / 2 years of service

Compensation expenses=480,00/2 years of service

Compensation expenses= = 240,000

Therefore what Kat should recognize as compensation expenses is 240,000

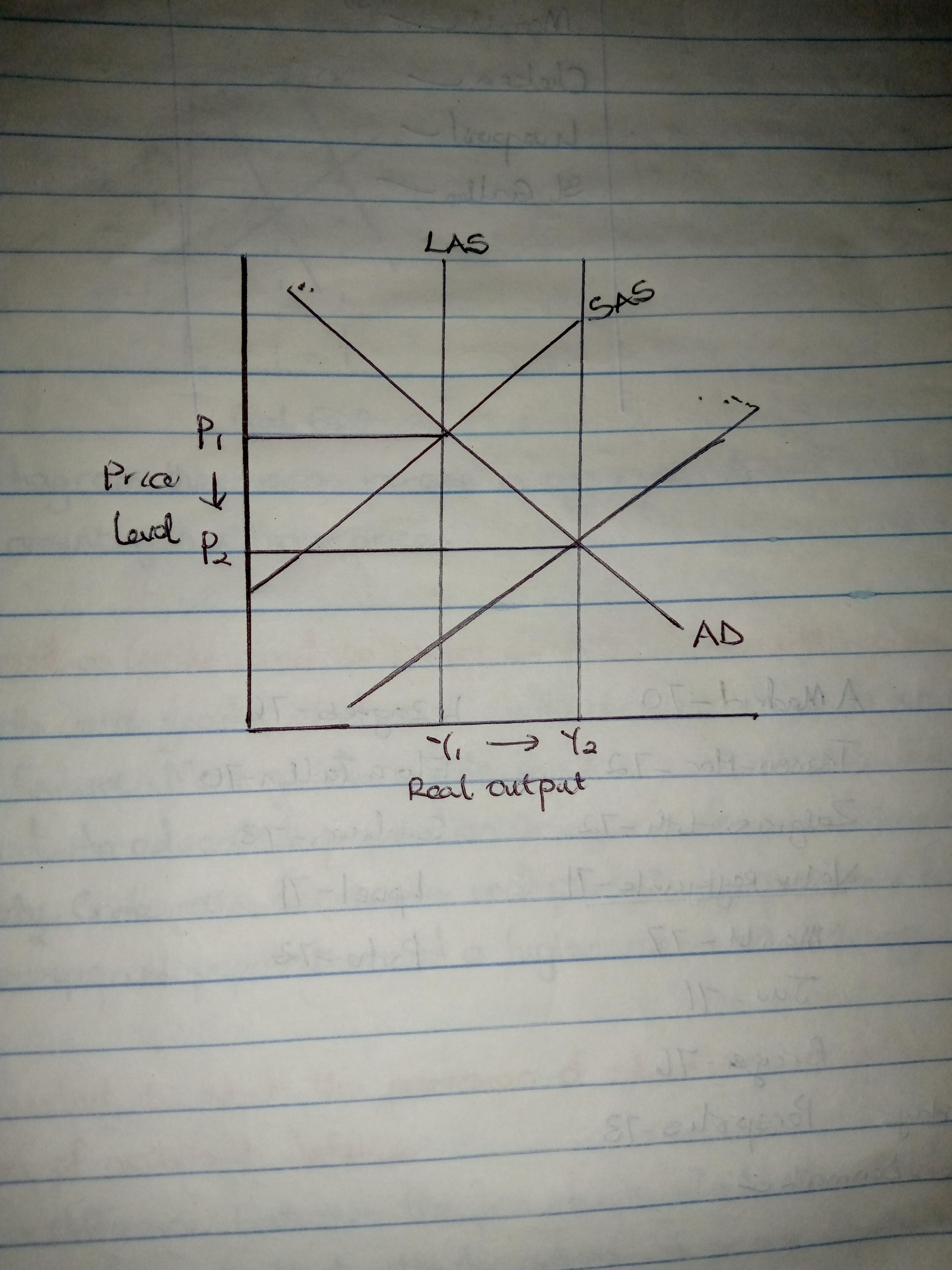

Answer: The price level falls and output rises.

Explanation:

According to Moore's law, it is stated that the computing speed of a microchip doubles every 18 months. According to Moore, this will increase thespeed and capability of computers and also bring about lesser pay for the computers.

The effect of this on the economy is that it will lead to a fall in price level and increase in output as there will be faster and cheaper production. This can be shown in the diagram attached.

Should be 21 days but that is not all the time!