Answer:

The correct answer is inject cash into it.

Explanation:

Every day, central banks lend money to private banks through auctions. The extraordinary thing about these new liquidity injections starring the European Central Bank or the US Federal Reserve is not so much the operation itself, as the situation in which they occur.

In this case, problems arise when, due to distrust, banks do not lend money to each other, operations that are common when the system is working properly.

With extraordinary placements, the central entities replace that lack of funds that private banks have not been able to obtain from their partners and, at the same time, at a cheaper price - at a lower interest rate.

Answer:

10.03%

Explanation:

Using the dividend discount formula, find the cost of equity; r

whereby,

D1 = Next year's dividend = 5.29

P0 = Current price of the stock = 79.83

g = growth rate of dividends = 3.40% or 0.034 as a decimal

Next, plug in the numbers to the formula above;

As a percentage, r = 10.03%

Therefore, the company's cost of equity is 10.03%

Standard Oil

This was an American oil company that was into everything oil from refining to even the transportation, It was set up in 1870 by John D. Rockefeller as an organisation in the state of Ohio, it was the biggest oil refinery both home and abroad as at that time.

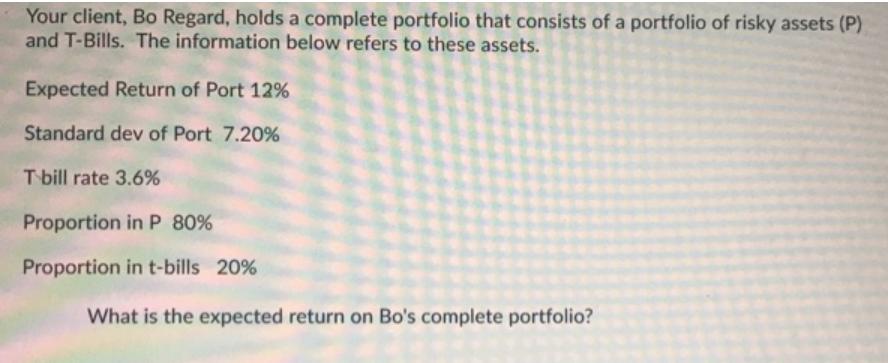

Answer:

The expected return on Bo's complete portfolio will be "10.32%".

Explanation:

The given question is incomplete. Please find attachment of the complete question.

According to the question, the given values are:

Port's expected return,

T-bill's expected return,

Port's weight,

T-bill's weight,

Now,

The Bo's complete portfolio's expected return will be:

⇒

On substituting the given values, we get

⇒

⇒

Note: percent = %

Answer:

The correct answer is A. One of the benefits of the current pattern of global trade is that consumers pay lower prices for goods and services.

Explanation:

Today, globalization has expanded international markets, interconnecting nations and their economies through free trade agreements, tariff elimination agreements and even through the transfer of companies from developed countries to peripheral countries, generating work in these nations and lowering production costs that allow reducing prices. All this allows consumers to access goods and services at a much lower cost than they previously accessed, thus reducing the amount they dedicate to consumption and thus increasing the performance of their wages, even allowing poverty reduction and a greater quality of life for people.