Answer:

Bail

Explanation:

Bail is just a measure of cash that is saved with the court to guarantee that you appear for all court procedures. You can post your bail in real money with the court, and you will at that point be discharged from authority.

In the event that the litigant needs more money to post the whole bail, the court will acknowledge a bail security.

The reason for bail is to guarantee that a respondent returns for future court appearances.

Answer:

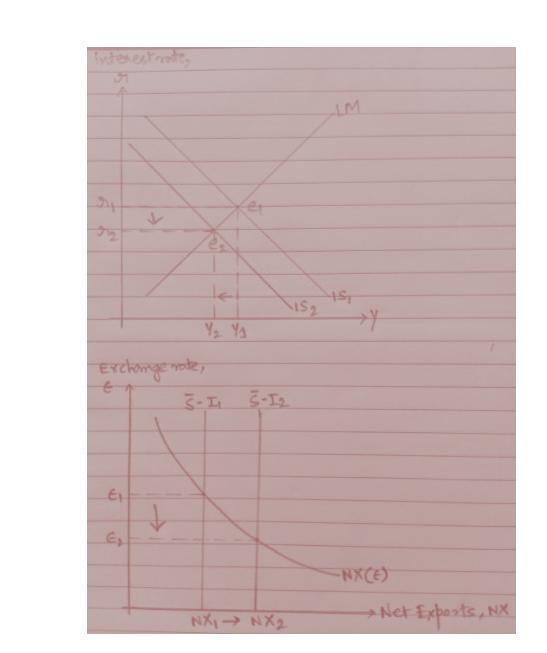

Following are the response to the given question:

Explanation:

Investing price falls as companies become increasingly negative about investment. Lowering prices for capital will shift the expenditure curve. When total expenditures drop, the IS curve moves to the left. It will lead to a decline in productivity and interest rates in the context of the IS-LM model. Next, consider how the current account will operate (which is the trade balance of the nation). This is what we're seeing as just a paradigm for just a real balance of currency fluctuations. The S-I line swings from S-I1 to S-I2 as expenditures decline from I1 to I2. The currency rate is down and private consumption has risen. Its idea is that even the currency is little valuable as exchange rates decline. Exports to the rest of the world are thus cheaper. Foreign exchange is appreciated as well as the domestic market needs costlier goods. Exports will therefore decrease. Export growth and import reductions are going to improve the trade balance. It will boost the bank account.

Answer:

D

Explanation:

time-series plot is a data visualization graph that illustrates data points at successive intervals or time.

Answer:

is based on the concept of just-in-time.

Explanation:

Supply chain management can be defined as the effective and efficient management of the flow of goods and services as well as all of the production processes involved in the transformation of raw materials into finished products that meet the insatiable want and need of the consumers.

Generally, the supply chain management involves all the activities associated with planning, execution and supply of finished goods and services from the manufacturers to the consumers.

Additionally, all businesses tend to use supply chain management to eliminate waste and maximize value for growth and development.

Hence, supply chain management is based on the concept of just-in-time (JIT) because it is a management framework that is focused on cutting manufacturing costs while increasing efficiency between suppliers and consumers through the use of a proper inventory system.