9514 1404 393

Answer:

- payment: $960.82; interest: $203,918

- balance: $317,306.36; interest: $227,306.36

Step-by-step explanation:

The sum of payments made n times per year for t years and earning annual interest rate r is the value of a single payment multiplied by k, where ...

k = ((1 +r/n)^(nt) -1)/(r/n)

__

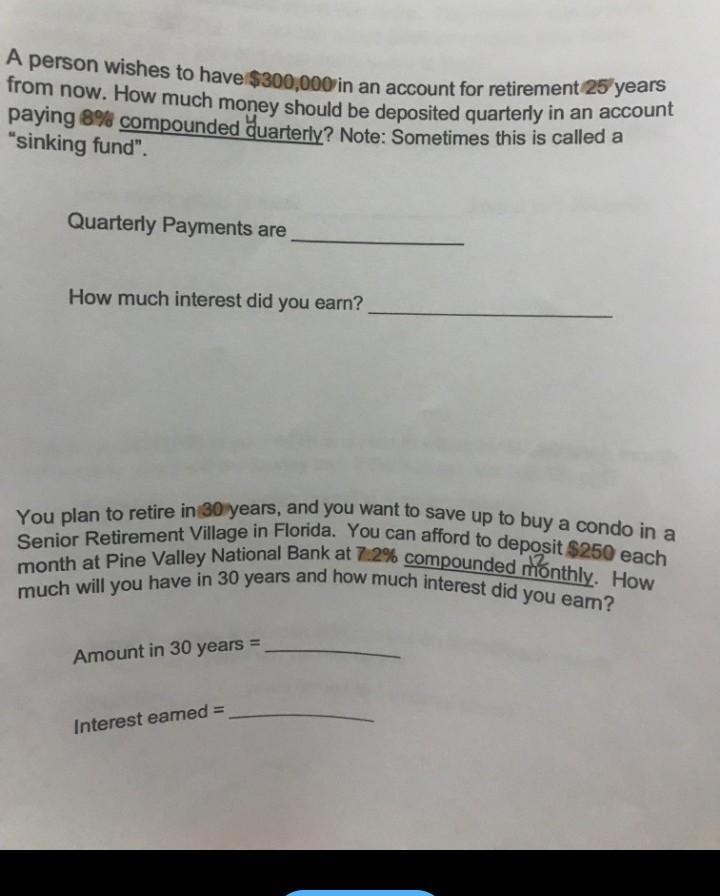

<u>Problem 1</u>

The multiplier k is ...

k = ((1 +0.08/4)^(4·25) -1)/(0.08/4) ≈ 312.232306

Then the quarterly deposit needs to be ...

$300,000/312.232306 ≈ $960.82

The sum of the 100 quarterly payments is ...

100 × $960.82 = $96,082

So, the amount of interest earned is ...

$300,000 -96,082 = $203,918

- Quarterly payments are $960.82

- Interest earned is $203,918

__

<u>Problem 2</u>

The multiplier k is ...

k = ((1 +0.072/12)^(12·30) -1)/(0.072/12) ≈ 1269.22544

Then the balance resulting from monthly deposits of $250 will be ...

$250 × 1269.22544 = $317,306.36

The total of the 360 payments is $90,000, so the interest earned is ...

$317,306.36 -90,000 = $227,306.36

- Account in 30 years is $317,306.36

- Interest earned is $227,306.36

_____

<em>Additional comment</em>

In the case of Problem 1, the deposit amount is <em>rounded down</em> to the nearest cent. This means that the account balance at the end of 25 years will be slightly less than $300,000. The difference is on the order of $0.96. This means both the account balance and the actual interest earned are $0.96 less than the amounts shown above.

In many of these school calculations, we ignore the effect of rounding the payment values. Similarly, we ignore the effect of rounding the account balance values for each monthly or quarterly statement. In real life, the final payment of a series is often adjusted to make up the difference caused by this rounding.

Also worthy of note is that the calculations here assume the payments are made at the end of the period, not the beginning. That makes a difference.