Answer:

Explanation:

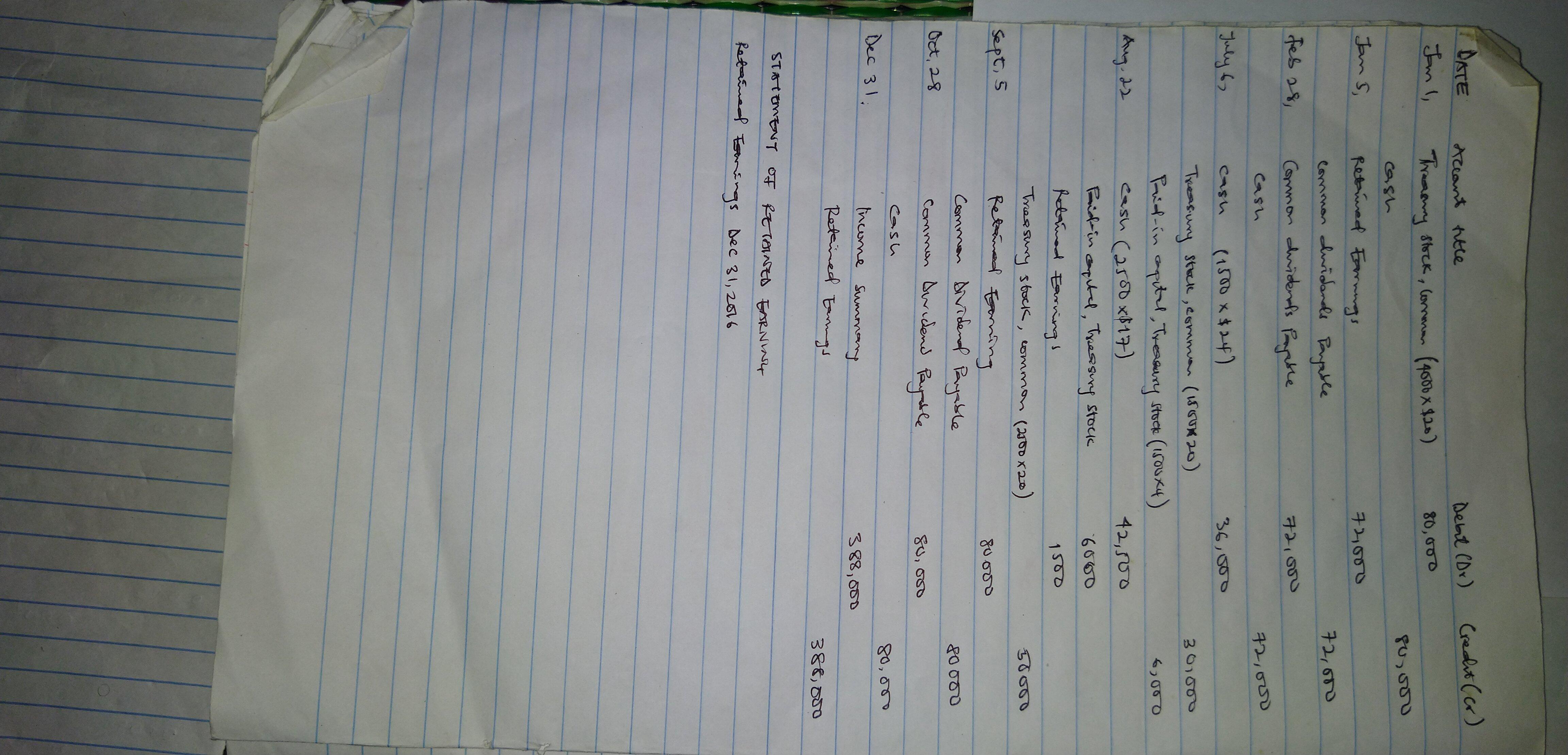

1.) Kindly check attached picture

2.) Statement of retained earning

Statement of Retained Earnings

For Year Ended December 31, 2018

Retained earnings, Dec. 31, 2017, 270,000

Add: Net income 388,000

Less: Cash dividends declared (152,000)

Less: Treasury stock reissuance (1,500)

Retained earnings, Dec. 31, 2018, 504,500

C.) Stockholders' Equity Section of the Balance Sheet

December 31, 2018

Common stock - $10 par value 400,000

Paid-in capital in excess of par value, common stock 60,000

Retained earnings 504,500