Answer:

The correct answers are;

Adult Care counselor - Sociologist

Nurse practitioner - Radiologist

Meeting Planner - Concierge

Explanation:

The question asks to correctly match the career with the different career groups. The adult care counselor can be a sociologist as he/she provides the services of counselling, human services, social work, give advice and help out in decision making.

Another career group is nurse practitioner which matches with the radiologist which diagnoses diseases and treats patients by imaging techniques. Example : X-Rays.

The third career group is meeting planner which perfectly classifies as concierge who is also known as a person who is a caretaker of a specific venue. He/She can assist guest or clients in booking a venue and arranging the events or meetings.

Answer:

Dysfunction

Explanation:

https://quizlet.com/346622755/final-exam-psychology-flash-cards/

There are three tools to achieve its monetary policy goals: the discount rate, reserve requirements, and open market operations

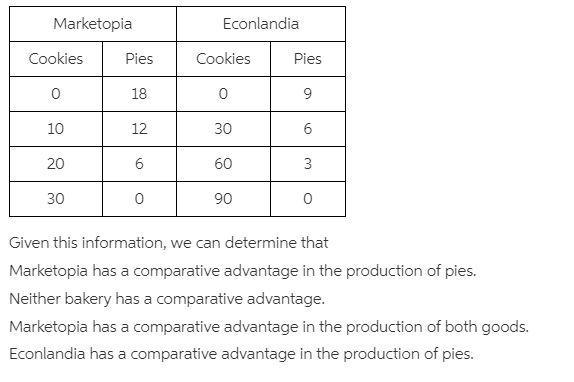

Answer: Marketopia has a comparative advantage in the production of pies.

Explanation:

The bakery with the comparative advantage in any of the goods is the one that has a lower opportunity cost in making it.

Marketopia.

Opportunity cost of Cookies = 18/30 pies = 0.6 pies

Opportunity cost of pies = 30/18 pies = 1.67 cookies

Econladia

Opportunity cost of Cookies = 9/90 pies = 0.1 pies

Opportunity cost of pies = 90/9 pies = 10 cookies

<em>It is shown that Marketopia has a comparative advantage in the production of pies because the opportunity cost of such is 1.67 cookies as opposed to Econladia which is 10 cookies. </em>

The most obvious benefit of specialization and trade is that they allow us to: <span>Consume more goods than we otherwise would be able to consume

When we do specialization, we could produce the goods that provide competitive advantage for us so we can produce that goods in a huge amount.

After that, we can trade the goods with other goods (which gives competitive advantage to other country) and trading countries could consume goods on a huge amount.</span>