Answer:

McDonalds reacts ethically as an example

Explanation:

Hope it helped

Answer:

the capital gain for the first year is $23.15

Explanation:

The computation of the capital gain for the first year is shown below;

Current value = Future dividend and value × Present value of discounting factor(rate%,time period)

= $1.4 ÷ 1.1 + $1.5 ÷ 1.1^2 + $25 ÷ 1.1^2

= $23.15

Hence, the capital gain for the first year is $23.15

The same should be considered and relevant too

Answer:

Production= 455,000 units

Explanation:

Giving the following information:

Beginning Inventory= 81,000

Ending Inventory= 51,000

Sales= 485,000

<u>To calculate the production required for the period, we need to use the following formula:</u>

Production= sales + desired ending inventory - beginning inventory

Production= 485,000 + 51,000 - 81,000

Production= 455,000 units

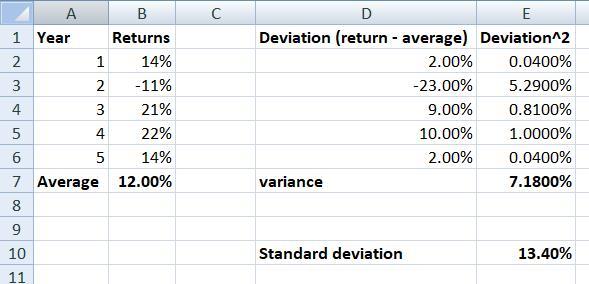

Answer and Explanation:

The calculations of the stock return for the missing year is shown below:

a. Let us assume the fifth year stock return be x

As we know that

Average rate of return = Total returns ÷ number of years

0.12 = (0.1 - 0.11 + 0.21 + 0.22 + x) ÷ 5

So after solving this, the x is 14%

b. Now the standard deviation of the stock return is presented in the excel spreadsheet

The standard deviation is 13.40%

i would say its either B or C...but imma go with the answer C