For your answer it’s letter c Because Providing incentives for customers to learn more about your services is known as Permission marketing

Answer:

The correct answer is letter "A": nonequivalent group.

Explanation:

While conducting studies, nonequivalent groups are those where the target audience is not selected randomly. Instead, the participants are chosen generating another group represented by all those individuals who match the research criteria but, because of a reason, were not selected.

<em>There are different types of nonequivalent groups such as posttest only nonequivalent groups or pretest-posttest nonequivalent groups, for instance.</em>

Answer:

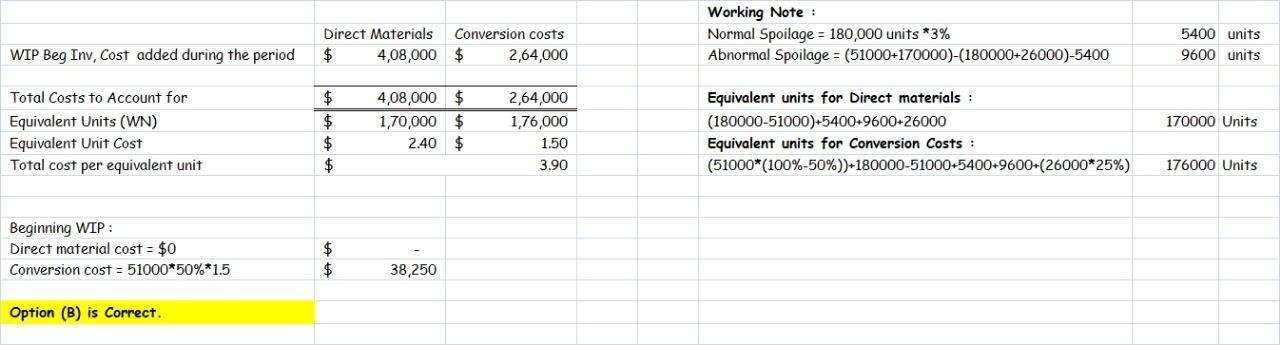

Below in the attached image is a well formatted solution to the above question as required

Answer:

Open

Explanation:

Open shop arrangement is the term which is defined or described as the office, factory or other kind of business establishment in which the union, which is selected or elected through a majority of the employees, that later act as the representative of all the employees while making the agreements with the employer.

So, in this case, the Hector is against the or opposed ton unions. Therefore, the comments of the Hector states that he is in favor of an open shop arrangement.

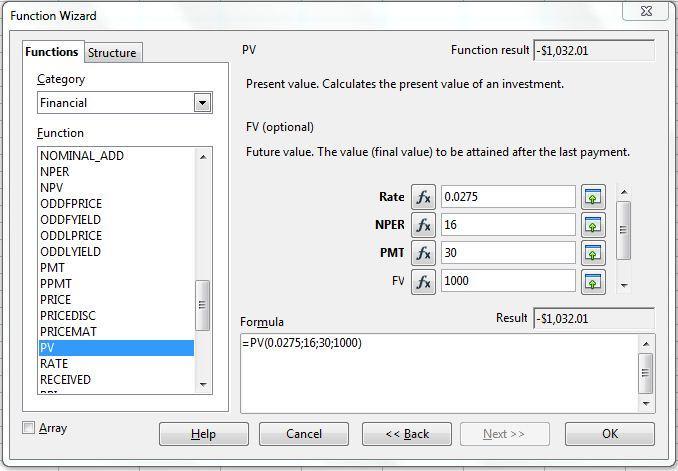

Answer:

$1,032.01

Explanation:

Given:

Face value of bond (FV) = $1,000

Coupon rate = 6% annual rate or 6% / 2 = 3% semi-annual rate

Coupon payment (pmt) = 0.03 × $1,000

= $30

Rate = 5.5% annually or 5.5 / 2 = 2.75%

Time period (nper) = 8 × 2 = 16 periods

Current value of bond is present value of bond which can be computed using spreadsheet function =PV(rate,nper,pmt,FV)

So, present value of bond is $1,032.01.

PV is negative as it's cash outflow.