Answer:

hedonic Theory of Wages:

Accept just two kinds of occupations in the work showcase (safe employments versus unsafe occupations). Under this, sheltered employments have likelihood of zero that specialist gets harmed. Unsafe occupations have likelihood of 1 and laborers know this. Laborers care about whether their occupations are sheltered or hazardous.

Laborers expand utility by picking wage-chance blends that offer them the best measure of utility. Expect laborers disdain hazard, yet to various degrees, for example they have diverse ideal pay chance blends. Firms are on their isoprofit bends that give the hazard wage mixes that give zero (financial) benefit. They vary between firms. An indulgent pay work mirror the connection among wages and occupation qualities. It matches laborers with various hazard inclinations with firms that can give employments that coordinate these diverse hazard inclinations.

Apathy bends uncover the exchange offs that a laborer favors among wages and level of hazard (chance thought to be an 'awful'). To give a similar utility, dangerous occupations must compensation higher wages than safe employments. The more prominent the laborer's aversion for hazard, the more prominent the pay off required for changing from a safe to an unsafe activity, and the more noteworthy the booking cost. As the pay firms bring to the table for hazardous occupations increments, less firms will extend to dangerous employment opportunities and bringing about a descending slanting interest bend as it turns out to be increasingly productive for firms to make occupations spare than to pay the higher compensation.

Suppositions of Differential Wage Theory are:

- The compensation differential is sure. Hazardous employments pay more than spare occupations.

- The balance wage differential is that of the last laborer employed (the peripheral specialist). It's anything but a proportion of the normal abhorrence for chance among laborers in the work showcase.

- Along these lines, everything except the minimal specialist are overcompensated by the market.

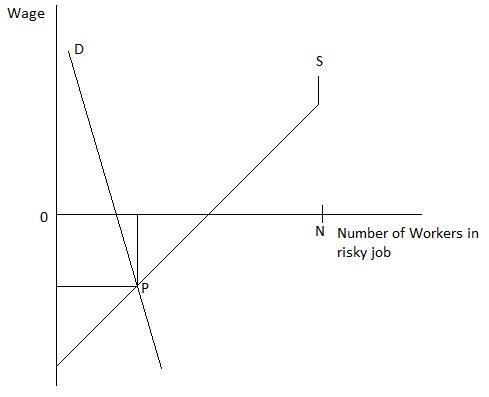

On the off chance that a few specialists like to work in dangerous occupations (they are eager to pay for the option to be harmed) and if the interest for such laborers is little, the market repaying differential is negative. At point P, where supply rises to request, laborers utilized in unsafe occupations acquire not as much as laborers utilized in safe employments. The outline given beneath shows the circumstance:

Isoprofit Curve:

As it is exorbitant to create well-being, a firm contribution hazard level P* can make the working environment more secure for example move left on flat pivot, just on the off chance that it diminishes compensation while keeping benefits consistent, so that the iso-benefit bend is upward slanting. Higher isoprofit bend returns lower benefit.

Answer:

Allocated overhead= $266.66

Explanation:

The fixed machine cost would be allocated using an overhead absorption rate

OAR = Budgeted overhead for the period /Budgeted copies

= 2000/30,000

= $0.0667 per copy

Allocated overhead = OAR × actual copies produced

Allocated Overhead for Accounting department

= $0.0667 × 4,000

= $266.66

Answer:

The break even level of units per month fall by 16 units.

Explanation:

The current breakeven units per month are,

Break even in units = 5600 / (20 - 6)

Break even in units-March = 400 Units

The fixed costs remain constant in the short run to a certain activity level so assuming that the fixed costs will remain $5600.

The new variable costs will be 6 * 0.9 = $5.4

Assuming everything else remains constant,

The new break even in units per month = 5600 / (20 - 5.4)

New break even in units = 383.56 rounded off to 384 units

As a result of decrease in the variable cost per units, the new break even point becomes 16 units less than the previous one.

Answer:

Increasing dividends may not always increase the stock price, because less earnings may be invested back into the firm and that impedes growth.

Explanation:

if increasing dividends results in the company not having enough funds for reinvestment, then value of the company may go down, since value of a stock is the present value of all expected cash-flows from holding the stock. But, if the company is paying dividend from free cash flows, then the payment of the dividend will not negatively affect the value of the stock.

In summary, paying a dividend will not always increase the stock price, and will not always decrease the stock price.

You must look first for the probability of the 4 prizes

which are $500, $100, $25, and no prize.

P ($500 prize) = 1/100 or 0.01

P ($100 prize) = 2/100 or 0.02

P ($25 prize) = 4/100 or 0.04

P (No prize) = 100/100 – 1+2+4/100 =93/100 .93

Expected gain or loss is computed by: (P(x)* n)

E= (500-10)*.01 + (100-10)*0.02 + (25-10)* 0.04 + (-10)*.93

= 4.90 + 1.80 + 0.6 – 9.3

E = -2

There is a loss of $2.