Answer:

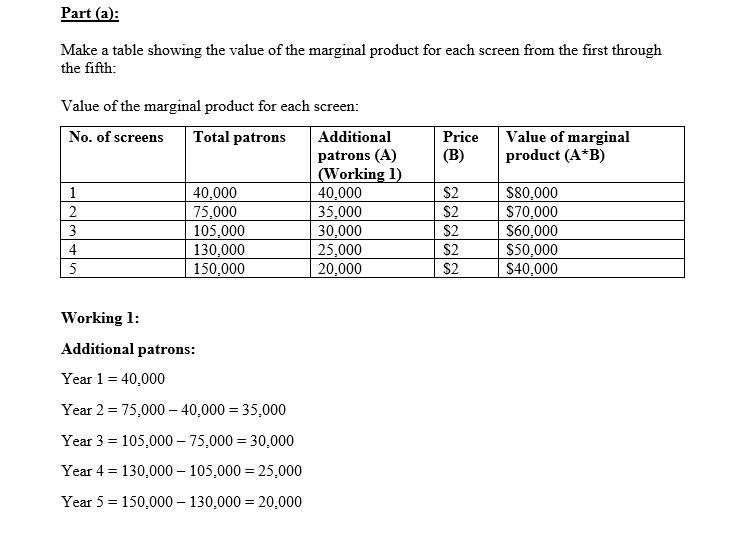

<u>Part (a):</u>

Make a table showing the value of the marginal product for each screen from the first through the fifth:

<u>Solution: </u>

The answer is attached.

<u>Part (b):</u>

How many screens will be built if the real interest rate is 5.5 percent?

<u>Answer:</u> 3 screens

<u>Part (c): </u>

How many screens will be built if the real interest rate is 7.5 percent?

<u>Answer:</u> 1 screen

<u>Part (d):</u>

How many screens will be built if the real interest rate is 10 percent?

<u>Answer:</u> 0 screens

<u>Part (e): </u>

If the real interest rate is 5.5 percent, how far would construction costs have to fall before the builder would be willing to build a five-screen complex?

<u>Answer:</u> $727,272.73(approx.)

Explanation:

Part (a):

Make a table showing the value of the marginal product for each screen from the first through the fifth:

Solution:

The solution is attached with working.

<u>Part (b):</u>

<u>How many screens will be built if the real interest rate is 5.5 percent?</u>

<u>Solution:</u>

3 screens

The interest cost of each screen = 5.5% x $1,000,000 = $55,000.

There are no other costs mentioned. The value of marginal product exceeds $55,000 for 3 screens.

Therefore, 3 screens should be built.

<u>Part (c): </u>

<u>How many screens will be built if the real interest rate is 7.5 percent?</u>

<u>Solution:</u>

1 screen

The value of the marginal product exceeds the interest cost (7.5% of $1,000,000, or $75,000) for only the first screen.

Thus, <u>one</u> screen will be built.

<u>Part (d):</u>

<u>How many screens will be built if the real interest rate is 10 percent?</u>

<u>Solution:</u>

0 screens

At 10% interest, the interest cost of a screen is $100,000, more than the value of the marginal product of even the first screen.

<u>

</u>Thus, no screens will be built.

Part (e):

<u>If the real interest rate is 5.5 percent, how far would construction costs have to fall before the builder would be willing to build a five-screen complex?</u>

<u>Solution:</u>

The value of the marginal product of the fifth screen is $40,000. At an interest rate of 5.5%, building five screens is profitable only if 5.5% times the per-screen construction cost is no greater than $40,000.

<u>Financial cost per screen = real interest rate x construction cost of per screen

</u>

$40, 000 = 5.5% x construction cost per screen Construction cost per screen = $40,000 ÷ 5.5%

= $727,272.73(approx.)

<u></u>