Answer:

True

Explanation:

The salary is paid to employees which means that the benefits that the employee receives by delivering its services is labor cost to the company. The company pays its employees to receive the desired services that the employee is willing to deliver its employer.

Answer:

all of the above

Explanation:

<u>Decision support systems</u> is a computer system that uses information systems. <em>The main objective</em> of this program is to assist in organizational decision making. To be enabled for this function, the system operates using a large amount of data, which converts information and compiles the most relevant information to provide existing alternatives that assist the effective decision making process.

Answer:

Which of the following statements is false?

a. Actual overhead costs always enter the Work-in-Process account.

Explanation:

a. Actual overhead costs always enter the Work-in-Process account.

A normal job-order costing system is a system that uses: Actual costs for direct materials and direct labor and estimated costs for overhead. Actual overhead costs are not assigned directly to jobs

b. The use of normal costing means that overhead is applied to each job using a predetermined rate.

The cost of a job includes direct materials, direct labor, and applied overhead. The use of normal costing means that overhead is applied to each job using a predetermined rate.

c. Indirect labor is assigned as a part of overhead.

Since direct materials and direct labor are usually considered to be the only costs that directly apply to a unit of production, manufacturing overhead is (by default) all of the indirect costs of a factory. Manufacturing overhead does not include any of the selling or administrative functions of a business

Answer:

The amount of depreciation expense on the consolidated income statement is $144,375

Explanation:

The computation of the depreciation expense is shown below:

Excess depreciation arise on gain on sale of asset is

= ($125,000 - $80,000) ÷ 8 years

= $5,625

Now the Consolidated depreciation is

= $86,000 + $64,000 - $5,625

= $144,375

Hence, the amount of depreciation expense on the consolidated income statement is $144,375

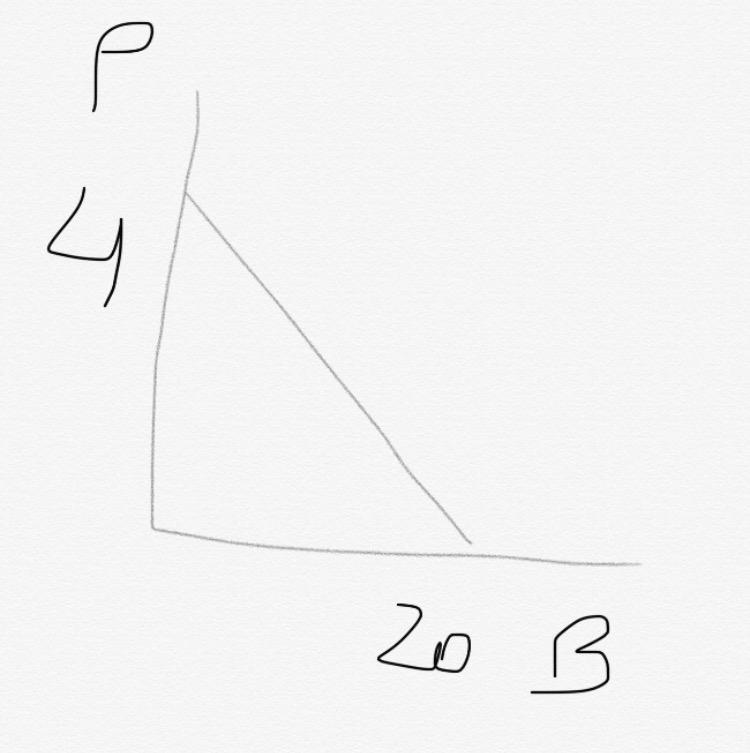

Answer:

First 4 subparts are answered below:

A)

Equation for budget constraint: p1.x1 + p2.x2 = M

Substituting the given information gives: 1B + 5P = 20

B)

The budget constraint is below: See attachment

C)

Slope of budget constraint: -P(pizza)/P(beer) = -5

D)

New budget constraint: 2B + 5P = 20

New slope: -5/2 = -2.5

New constraint line: See attachment