Answer:

Waldman Associates

Waldman does not have a contract for purposes of revenue recognition on the day the contract is received.

Explanation:

Revenue from contracts with customers becomes recognizable after the performance of the obligations and not before. Revenue is recognized when the contractor has transferred the benefits to the beneficiary and not before. Revenue, in this instance, is to be recognized based on past performance. According to IFRS 15 and ASC 606, revenue is recognized when each performance obligation has been fully satisfied. This is the point when economic benefit has been conferred on the other contracting party.

Answer:

9 years

Explanation:

Invoices and monthly statements are financial records of a company. Such records are subject to audit and tax queries. Typically, tax and audit queries arise after transactions and the financial year has been concluded. Sometimes, it may take years to conclude audit or tax queries.

Nine years is considered an ideal time to store such records. It is ample time to allow for any references to audit, tax, or any other query.

Answer: 0.35

Explanation:

The Price to Earnings ratio is used to value companies and is calculated by dividing the company's stock price by its earnings per share.

Earnings per share = 29,000,000/2,000,000 shares

= $14.50

PE ratio = Share price / Earnings per share

= 5.09/14.50

= 0.35

Answer:

Explanation:

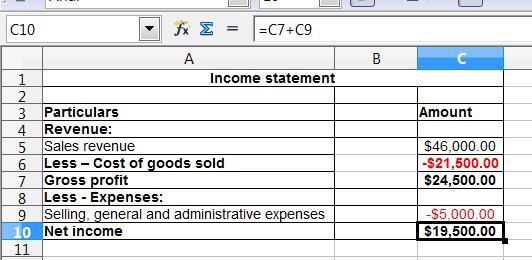

(a) The computation of the cost of goods sold is shown below:

= Beginning inventory + Purchase of new merchandise - ending inventory

= $4,000 + $22,000 - $4,500

= $21,500

(b) In the income statement, the total revenues and the total expenses are recorded.

If the total revenues are more than the total expenditure then the company earns net income

And, If the total revenues are less than the total expenditure then the company have a net loss

This net income or net loss would reflect in the statement of the retained earning account.

The preparation of the income statement is presented in the spreadsheet. Kindly find the attachment below: