Answer: None of the three tests were passed as the market transitioned.

Explanation: one of the core competencies of Kodak were

1. Film was the basics of their critics products and services. As the market transitioned from the use of films for camera and devices to digital, Kodak refused or was reluctant to take the necessary risk to expand and forge beyond it current market and product to the digitalized market as a result suffered the consequence.

Answer:

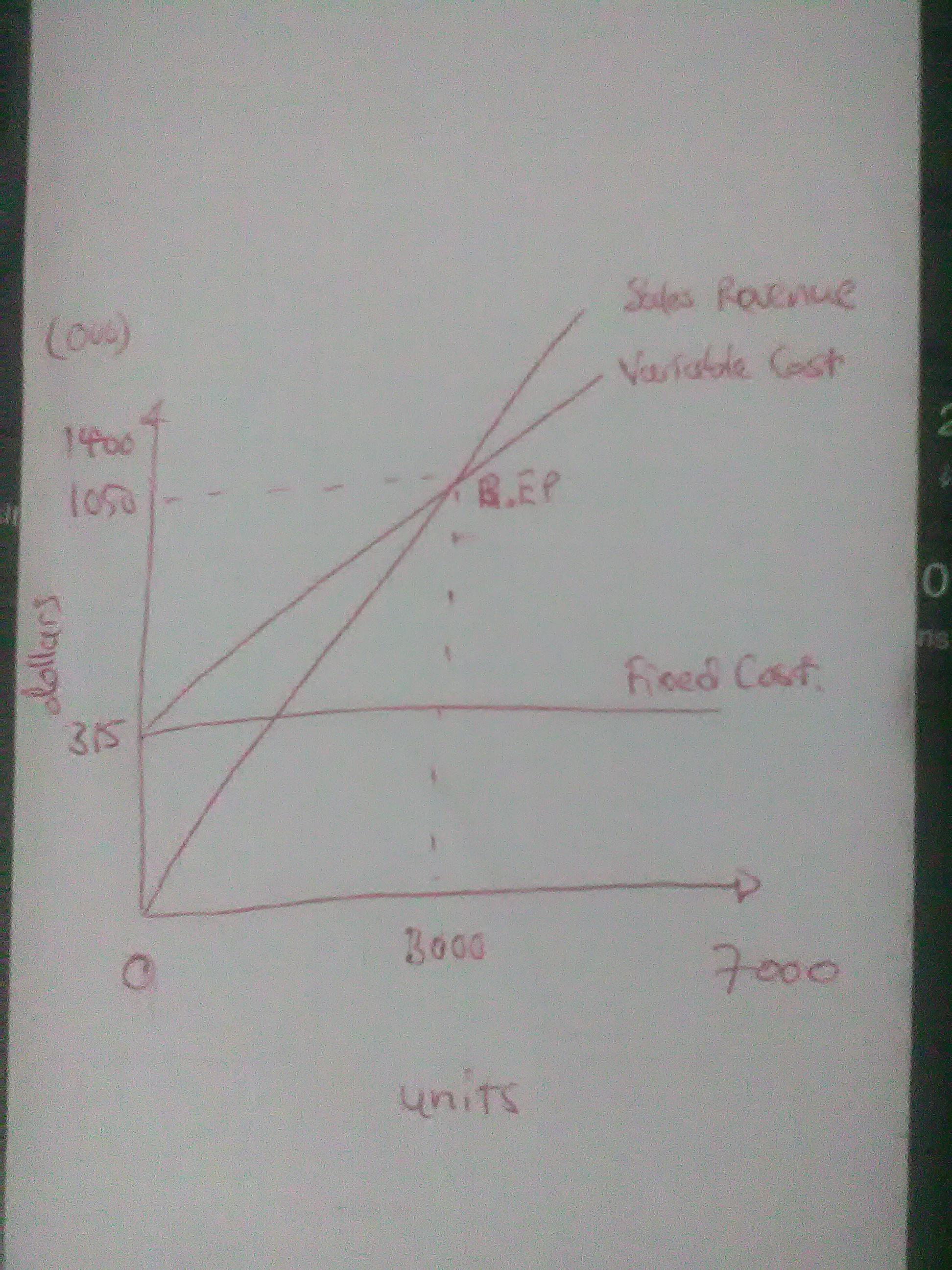

1a. 3,000 units

1b. $1,050,000

2. See attachment.

3. contribution margin income statement

Sales ($350 × 7,000 units) $2,450,000

Less Variable Cost ($245 × 7,000 units)) ($1,715,000)

Contribution $735,000

Less Fixed Costs ( $315,000)

Operating Profit $420,000

Explanation:

Break-even point (sales units ) = Fixed Cost ÷ Contribution per unit

= $315,000 ÷ ($350 - $245)

= 3,000

Break-even point (sales dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $315,000 ÷ ($105/$350)

= $1,050,000

Answer:

True.

Explanation:

In word processing software, there will be a default style applied to all text that can then be modified to fit your document.

Answer:

The correct answer is (A)

Explanation:

Normally, goods which close substitutes tend to have more elastic demand as it is easier to switch from one brand to another because they are close substitutes. For example, if the price of Pepsi increases the consumers will easily shift towards Coca-Cola. So, close substitutes are price sensitive and they have high elastic demand compared to other goods.

Answer:

$293,000

Explanation:

The computation of the product cost is shown below:

= Direct material + direct labor + factory supplies + factory depreciation + indirect labor

= $126,000 + $99,000 + $9,000 + $33,000 + $26,000

= $293,000

The factory supplies + factory depreciation + indirect labor = manufacturing overhead

All other cost are not relevant for the computation part. Hence, ignored it