Answer:

ANSWER:FALSE

Explanation:

LO: 02-04 Determine if an at-will employee has sufficient basis for wrongful discharge.

Topic: Employment-At-Will Concepts

Blooms: Apply

Difficulty: 2 Medium

AACSB: Reflective Thinking

Feedback: Hannah can file a wrongful discharge lawsuit against Friendly Catering Company. If there is no express agreement or contract to the contrary, employment is considered to be at-will; that is, either the employer or the employee may terminate the relationship at her or his discretion. Nevertheless, even where a discharge involves no statutory discrimination, breach of contract, or traditional exception to the at-will doctrine, the termination may still be considered wrongful and the employer may be liable for “wrongful discharge,” “wrongful termination,” or “unjust dismissal

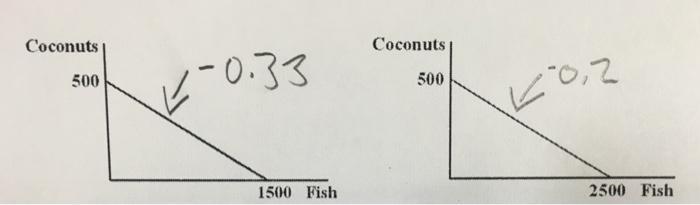

If you are offered 2 fish for every 1 coconut by the Island's delegate then you will reject it because it cost more than 2 fish to make one coconut.

<h3>What should you do about the island delegate's offer?</h3>

In order to make one coconut, the number of fish that you give up are:

= 1500 / 500

= 3 fish

The Island's delegate is therefore offering you less fish than what it costs to produce a coconut so you should reject the offer.

First part of question is:

This problem has been solved!

See the answer

You are the Minister of Trade for a small island country in the South Pacific with the annual production possibilities curve depicted below on the left. You are negotiating a deal with a neighboring island that has the annual PPC depicted below on the right:

Find out more on terms of trade at brainly.com/question/17727564

#SPJ1

Iran, is the country that borders the Caspian sea, the Persian gulf, and the gulf of Oman.

<h3>Which countries lie along the Caspian sea, the Persian gulf and the gulf of Oman?</h3>

Iran country lies in the Middle-East of the Iraq and Pakistan, that borders the Caspian sea, the Persian gulf, and the gulf of Oman.

The inland sea is connected to the Gulf of Oman from the East and the countries that lie along the Persian Gulf and the Gulf of Oman are Oman, Iraq, Kuwait, Saudi Arabia, etc.

Strait of Hormuz connects the the Persian Gulf to the Arabian Sea.

Learn more about the Persian gulf and the gulf of Oman here:-

brainly.com/question/4694666

#SPJ1

It is false that the allocation of approximately 20 minutes to answer the questionnaire will allow to achieve the most accurate snapshot of their likes and dislikes on the consumer preferences survey.

The method of data collection used in this case is known as Questionnaire.

- The number of minute used by respondent to answer question on the questionnaire does not determine the accuracy of their inputs.

In conclusion, It is false that the allocation of approximately 20 minutes to answer the questionnaire will allow to achieve the most accurate snapshot of their likes and dislikes on the consumer preferences survey.

Read more about Respondent:

<em>brainly.com/question/18151532:</em>

<em />

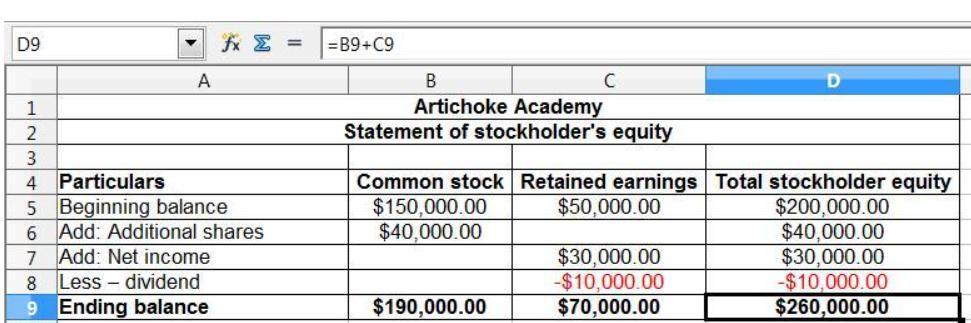

Answer and Explanation:

The preparation of the statement of the stockholder equity and balance sheet would be shown in the attachment below:

The formulas for ending retained earning balance and stockholder equity is

Ending retained earnings = Opening retained earnings + net income - dividend paid

And, the ending equity is

= Opening equity + additional shares

The same would be shown in the attachment