Answer:

Since the calculated value of F= 5.733 falls in the critical region we reject the null hypothesis and conclude all three means are not equal.

Explanation:

The given data is

Banking Retail Insurance

12 8 10

10 8 8

10 6 6

12 8 8

<u>10 10 10</u>

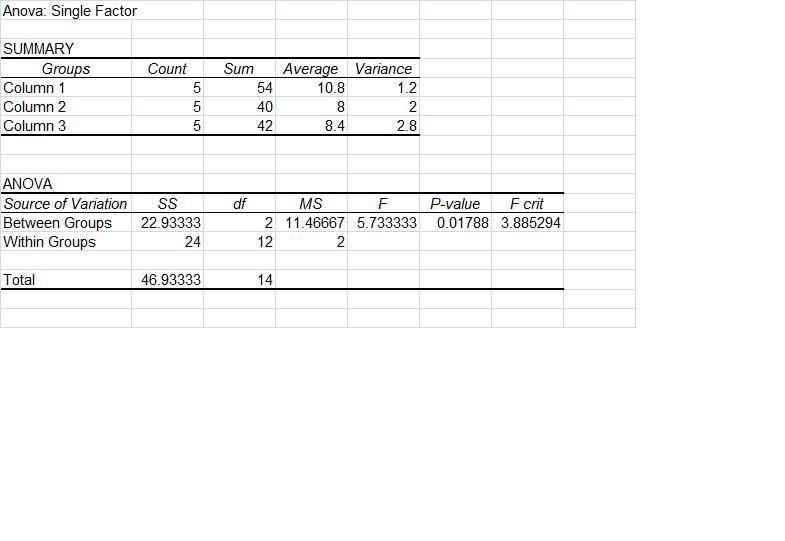

The results of excel are:

<u><em>Anova: Single Factor </em></u>

SUMMARY

Groups Count Sum Average Variance

Column 1 5 54 10.8 1.2

Column 2 5 40 8 2

Column 3 5 42 8.4 2.8

1) Let the null and alternate hypotheses be

H0: u1=u2=u3 i.e all the three means are equal and

Ha: Not all three means are equal

2) The significance level is set at ∝ =0.05

3)The test statistic to use is

F= sb²/ sw²

which has F distribution with v1= k-1 →3-1=2 and v2= n-k →15-3=12 degrees of freedom

After calculations the following table is obtained.

<u><em>ANOVA </em></u>

Source SS df MS F P-value F crit

of Variation

B/w Groups 22.93 2 11.467 5.733 0.01788 3.885

<u>Within Groups 24 12 2 </u>

<u>Total 46.93 14 </u>

4) The critical region is F ≥ F(0.05, 2,12) = 3.885

5) Since the calculated value of F= 5.733 falls in the critical region we reject the null hypothesis and conclude all three means are not equal.