Keynesian economists believe: <span>government can implement policy proposals that can positively impact the economy

Keynesian economist generally believed that the Economic situation in a country is a direct result from both private and public sector activities simultaneously, so both positive and negative things could derive from both sectors</span>

Based on the discount offered and the cost of advertising, your budget variance is <u>$500 </u>and it is a <u>surplus</u>.

<h3>How much do you spend on advertising?</h3>

You need to advertise for 6 months which means that you will pay for two three-month advertising seasons.

The first season will cost $2,000 because of the discount and the second season will cost $2,500. Total cost is:

= 2,000 + 2,500

= $4,500

<h3>What is the Budget surplus?</h3>

= Budget - Amount spent

= 5,000 - 4,500

= $500

Find out more on budget variance at brainly.com/question/25625268.

Answer:

d. beta did a better job of explaining the returns than standard deviation

Explanation:

Beta measures the systemic risk associated with the particular investment, it do not compute the total risk associated, which is more logical.

Standard deviation computes the total risk associated.

Some risk is natural, like the risk of floods, natural calamities, earthquake, etc:

That risk shall not counted as for comparison as that is associated universally. Further, the risk associated with particular factors like bankruptcy of a company, or some legal case issue of a company are precisely described by beta coefficient.

Thus, beta provides better details about explaining the returns.

Answer :

A blade ignition key to start the engine.

Remote keyless entry to lock or unlock the doors

Answer:

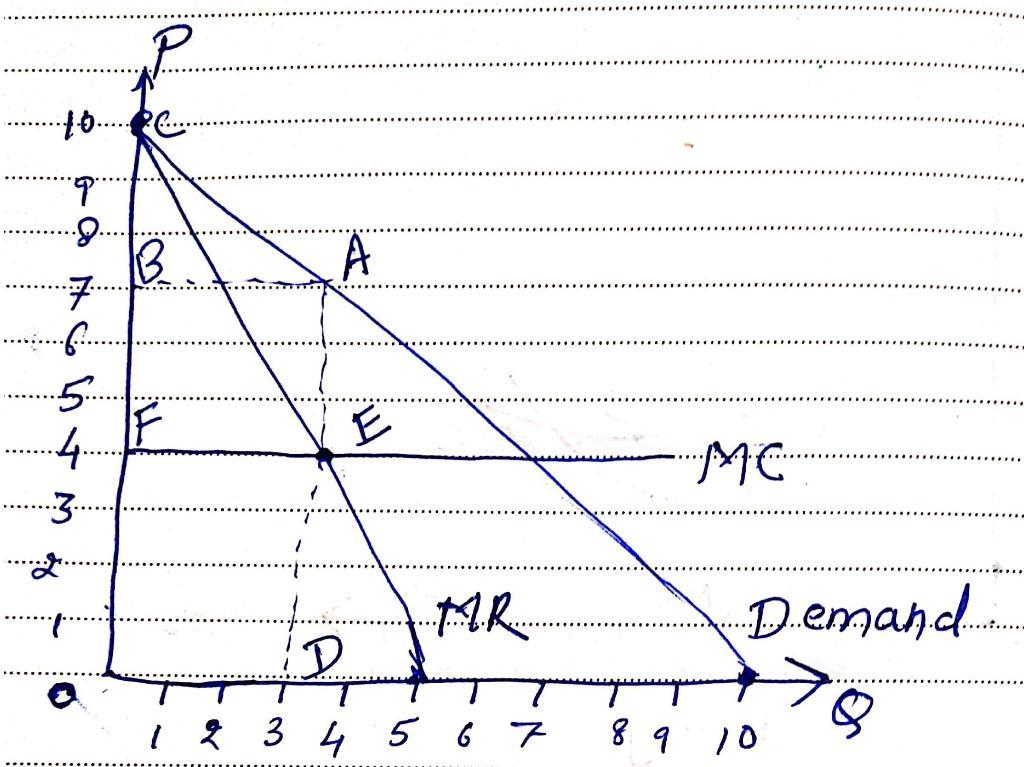

1 (a)

Since p = 10 - Q,

Revenue = p × Q=10Q - Q2

Hence, MR = 10 - 2Q.

MC is given fixed at 4.

Demand function is Q = 10 - p.

Plotting all these values in graph attached picture, we get

1 (b)

The monopolist will yield where MR = MC. So,

10 - 2Q = 4

Q = 3.

At this quantity, P = 7.

1 (c)

Consumer Surplus = Area of Triangle ABC = 0.5 × 3 × 3 = 4.5

Producer Surplus = Area of Rectangle ABEF = 3 × 3 = 9

2 (a)

Since the price is now P = MC = 4, this means

Q = 10 – 4 = 6.

2 (b)

The consumer surplus in this case would be = 0.5 × 6 × 6 = 18

The producer surplus will be zero.

2 (c)

Deadweight Loss = Total Surplus in Case B - Total Surplus in Case A

18 - 13.5 = 4.5