Answer and Explanation:

a. The computation is shown below;

Cash bonus after tax is ($3,000 × (1 - 0.24) $2,280

And, non taxable fringe benefit is $2,300

So here he should use the nontaxable fringe benefit

b. Yes answer would be changed

Cash bonus after tax is ($3,000 × (1 - 0.12) $2,640

And, non taxable fringe benefit is $2,300

hence, the same is to be considered

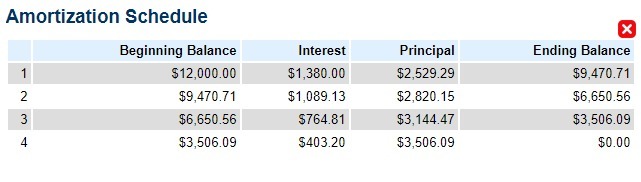

Answer: $403.20

Explanation:We use a mortgage calculator to calculate the interest paid in the final payment. Since each repayment is made at the end of year, the repayments are annual payments. So, the calculator should have an annual amortization schedule to solve the problem.

I used

http://www.calculator.net/loan-calculator for the calculation because it has an annual payment schedule. Then, I went under the subtitle

Paying Back a Fixed Amount Periodically because the payments are equal. In that online calculator, I just input these data:

- Loan Amount: $12,000

- Loan Term: 4 (Loan term is number of years to pay the loan)

- Interest Rate: 11.5%

- Compound: Annually (APY)

- Pay Back: Every year

Then, I clicked the

calculate button and view amortization table. The annual amortization schedule is attached in this answer.

To determine the interest paid at the final payment, I looked at payment #4 because the final payment is at the 4th year. (The loan is paid in 4 annual payments).

As seen in the attached image, the interest paid in payment #4 is $403.20. Hence, the interest paid in the final payment is

$403.20.

Answer:

$320,000 or $0.32 million

Explanation:

In accounting, the percentage of bad debt expenses is applied to the outstanding accounts receivable at the end of a particular accounting period.

In the question, the end of the accounting period is given as December 31 and the outstanding accounts receivable as at that December 31 is a total of $6.40 million. Therefore, we will disregard other values and simply apply 5% to the the outstanding accounts receivable of $6.40 million as at that December 31 as follows:

Bad debt = Outstanding accounts receivable × 5%

= $6.40 million × 5%

= $6,400,000 × 5%

= $320,000

Therefore, the amount of bad debt expense to recognized for the year is $320,000 or $0.32 million.