Answer:

38,000 units

Explanation:

Total production required = Forecasted unit sales + Planned finished goods inventory balance = 36,000 + 14,000 = 50,000 units

Products to be manufactured = Total production required - Beginning finished goods inventory = 50,000 - 12,000 = 38,000 units

The number of finished units to be produced = 38,000 units

So the correct answer will be 38,000

Answer:

1.

Dr Bonds 940,000

Cr Cash 940,000

Dr Fair Value adjustment 45,000

Cr Net Unrealized holding gains & losses 45,000

2.

Dr Fair Value adjustment 45,000

Cr Net Unrealized holding gains & Losses 45,000

3.

Dr Investment in bonds 985,000

Cr Discount on bond investment 45,000

Cr Cash 940,000

Explanation:

Hoosier Company Journal entries

1.

Dr Bonds 940,000

Cr Cash 940,000

Dr Fair Value adjustment 45,000

($985,000-$940,000)

Cr Net Unrealized holding gains & losses 45,000

2.

Dr Fair Value adjustment 45,000

Cr Net Unrealized holding gains & Losses 45,000

3.

Dr Investment in bonds 985,000

Cr Discount on bond investment 45,000

Cr Cash 940,000

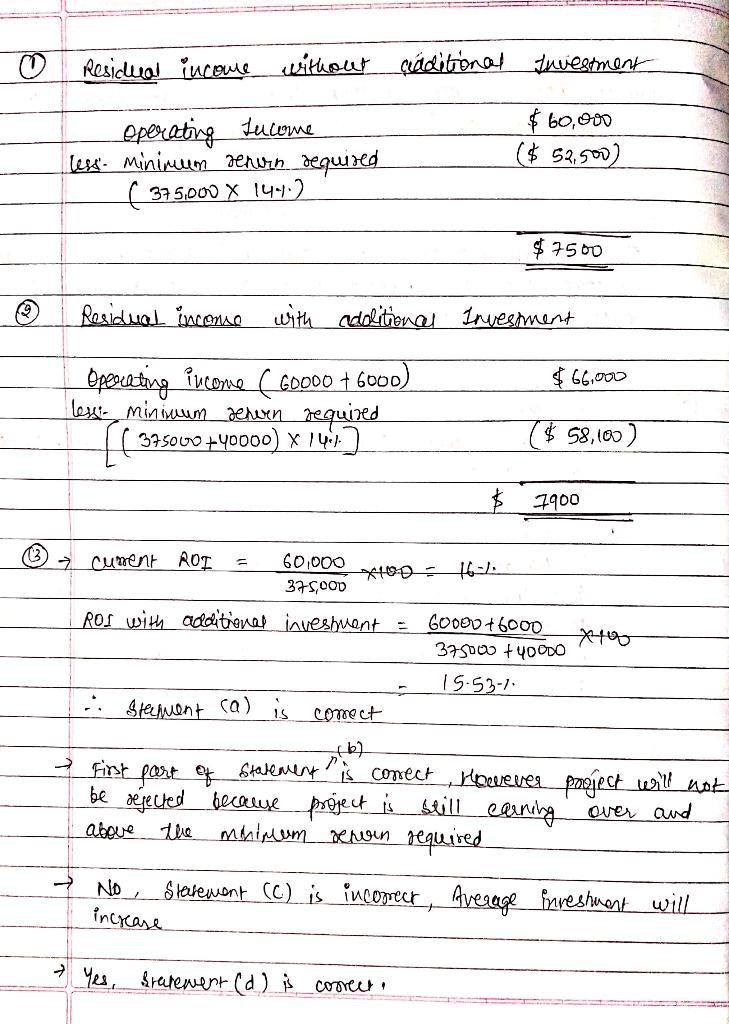

Answer:

d. If the manager invests in the additional project, residual income of the division will increase.

Explanation:

RI = Operating Income - (Operating Assets x Minimum Required Rate of Return)

with adding the additional project

Operating Income: $60000 +6000 =$66000

Operating Assets: $375000+$40000 =$415000

Residual income =$66000-14%*$415000 =$7900

Consider the attached information.

Answer:

b. 300,000 shares being sold is an issuer transaction and the 200,000 shares being sold is a non-issuer transaction.

Explanation:

A non-issuer transaction is a transaction that does not directly benefit an issuer or it was not directly executed to benefit an issuer.

According to the Uniform State Law, an entity involved in the sales of certificates of interest, leases, mining titles among others is officially exempted from being labelled as an issuer. Hence, the entity (officers of the firm) in the question are non-issuer brokers.

Specifically, when the sales of stock are carried out by someone or an individual who is not a registered stockbroker, that individual officially becomes what is called 'a non-issuer broker-dealer'. The implication is that such a transaction is to be exempted from the registration requirements of the Security Exchange Commission.

In this question, since the issuer newly issued 300,000 shares while the remaining 200,000 in the proposed combination was offered by Officers of the firm - non-issuer broker-dealers. The Law states that it must be separated to show that 300,000 shares are sold in an issuer transaction (Primary) directly involving an official issuer while 200,000 shares are sold in a non-issuer transaction (Secondary).

Answer:

Fixed and Variable cost:

Fixed cost are the costs which cannot be changed with change in the level of goods and services sold or produced.

Variable cost are the costs which changes with change in the level of output produced and sold.

Product and Period cost:

Product costs are the costs which are incurred for making the product such as direct material, factory overhead and direct labor, etc.

Period costs refers to the cost which are incurred for a certain period of time. It is normally associated with the time period than with any type of transactional event.

Therefore, the classification of items is as follows:

(a) Variable cost - Product cost

(b) Variable cost - Product cost

(c) Fixed cost - Period cost

(d) Fixed cost - Period cost

(e) Fixed cost - Period cost

(f) Fixed cost - Period cost

(g) Variable cost - Product cost

(h) Fixed cost - Period cost

(i) Fixed cost - Period cost